Introduction

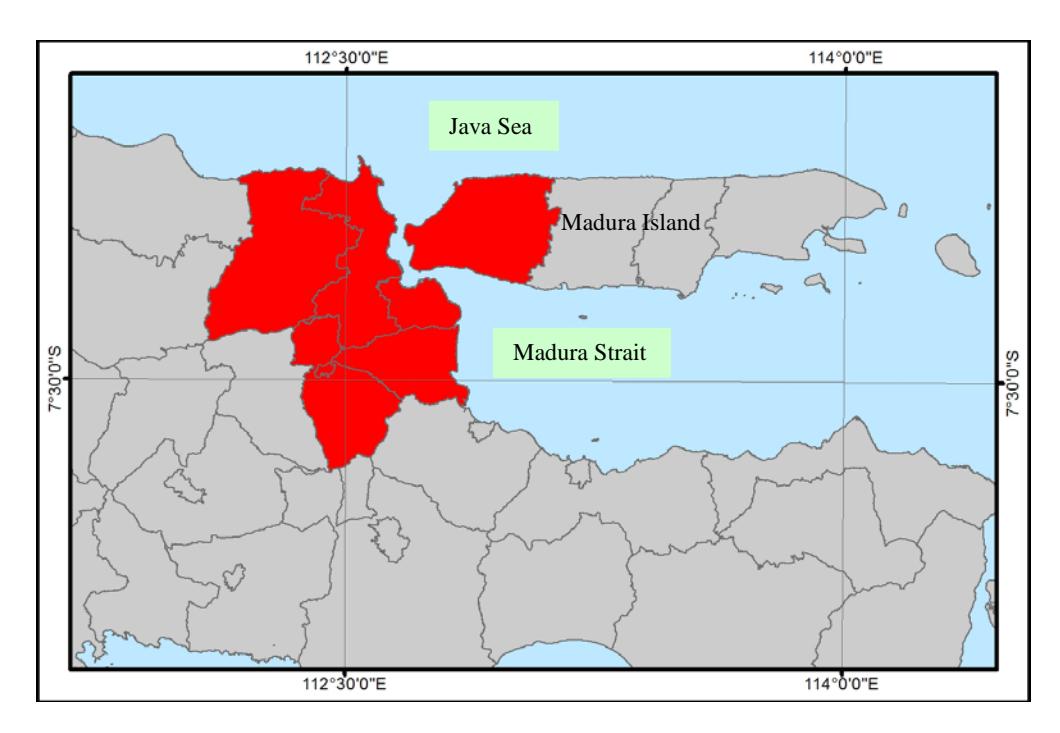

Gerbangkertosusila (GKS) is one of the national strategic areas (KSN) based on The Indonesian National Spatial Planning Document (RTRWN) 2008. The area consists of six municipal governments (Gresik, Bangkalan, Mojokerto, Surabaya, Sidoarjo, and Lamongan) and one provincial government (East Java province). Figure 1 shows in red the area covering all six municipalities. GKS KSN is intended to be a sustainable and global growth centre through the creation of logistics and a world economy window, as well as a smart and green metropolitan area (GKS Regional Plan: 2010-2030). The regional plan has 12 key strategic programs as shown in Table 1. Based on these programs, the main objective of GKS is to accelerate and coordinate the development process on the macro level and key strategic areas on the regional level.

Figure 1. Location of GKS KSN

In contrast, the development acceleration and coordination among the municipalities is still inadequate resulting in a slow development process (e.g. development around the Suramadu Bridge has not yet developed the surrounding areas as high-level commercial, industrial areas), regional disparities (e.g. Surabaya is in 3rd ranked while Bangkalan is 27th for economic growth in 2011), and unbalanced regional structure systems in some key regional projects (e.g. a debatable middle toll road in Surabaya can affect the performance of the GKS regional structure from the transportation aspect). Consequently, partnerships among the municipal and provincial governments are required to promote and control the development within GKS. Development control is needed to comply with all planning objectives in the GKS Regional Plan, particularly land use plan. Similar to spatial planning, development control also requires coordination among stakeholders. To implement the control, agreement on instruments of development control is ones of the key steps for successful partnerships among municipal governments, provincial governments, and the special body of GKS. Furthermore, a design for implementing the agreed instruments is required to have a successful partnership among related parties in GKS KSN.

Table 1. Key Strategic Program for GKS

| Category | Programs | |

|---|---|---|

| Infrastructure | • Development of Transport Infrastructure | |

| • Development of Water Resources Infrastructure | ||

| • Development of Wastewater and Urban Drainage | ||

| • Development of Regional Waste Infrastructure | ||

| • Energy | ||

| Area planning | • Development of Controlled Industrial Area | |

| • Development of Tourism Areas | ||

| • Development of Suramadu bridge area | ||

| Environment | Environment management | |

| Residences | • Development of a large-scale residential area | |

| • Settlements and social sector | ||

| Social | Strengthening social, culture, and economic sector | |

| Economic | ||

Source: GKS Regional Plan, 2010-2030

Methodology

Two main methods of data collection were conducted to finalize the agreed instruments, which are: questionnaire and focus group discussion (FGD). The questionnaire is designed to acquire information on the 60 instruments based on the literature review. Questionnaires are a wellestablished tool for acquiring information from participants on their social characteristics, present and past behaviours, standards of behaviour or attitudes, their beliefs and reasons for action with respect to the topic under investigation (Bulmer, 2004). The verification is conducted by assessing proposed instruments in terms of public policy criteria that are; effectively, efficiency, adequacy, responsiveness, accuracy, and equity (Dunn, 2000). In addition, the questionnaire also verifies the suitability of the instruments to be authorised in different levels of governments (municipal, provincial government or GKS body). The outputs of the questionnaire are possible adopted instruments in these three levels of government.

Furthermore, FGD focuses on reaching consensus on the possible adopted instruments. Questionnaires are more appropriate for obtaining quantitative information and explaining how many people hold a certain (predefined) opinion; focus groups are better for exploring exactly how those opinions are constructed (Robinson, 1999). The discussion enriches the outputs in the questionnaire process by finding common understanding on the possible adopted instruments from all the respondents. The output of FGD is called as agreed instruments for GKS development control.

To run both the questionnaires and FGD, a purposive sampling method is utilized to select appropriate respondents. The purposive sampling technique, also called judgment sampling, is the deliberate choice of an informant due to the qualities the informant possesses (Tongco, 2007). Since this study is limited to the bureaucrat perspectives on development incentives, we including numbers of bureaucrats from both levels (municipality and provincial level). At the current moment, there is no official ad hoc body for GKS KSN. In the bureaucrat system, the most relevant agencies for development control are regional planning board and permits agencies. Furthermore, since the issue of development control in GKS cuts across administrative boundaries, we have to include the cooperation agency as one of the key respondents. Therefore, we have a total of 21 agencies for 7 government authorities in KSN GKS. For the first stage, 13 respondents out of 21 invited respondents filled in the questionnaire. The questionnaire was designed for every municipality in GKS KSN. For every municipality, we targeted three main agencies, namely; the regional planning board, cooperation boards and permits agencies. For FGD as the second stage, we invited similar respondents from all municipalities in GKS KSN including East Java Province officers. 19 respondents out of the invitee were present and were divided into three main groups, namely: the group of planning implementation, planning permits and coordination-public relations. All respondents represented the two government levels for both processes of data collection. The FGD used a card-playing method to agree on possible instruments. We also asked a facilitator to manage the FGD process as well as to clarify the meaning of possible instruments.

Results

Proposed Instrument for Development Control Based On Literature Review

Proposed instruments of development control in GKS are compiled from policies, literature, and best practices. The Indonesian Regulation No. 15 in 2010 divides development control into four groups that are; zoning regulation, permits, development incentives and disincentives and sanctions. Therefore, the compilation on proposed instruments was grouped into those four classifications.

The provincial Government of Washington (USA) performs infrastructure management and rezoning to address spatial problems (Girling and Helpland, 2007). One of the incentives is to encourage job opportunities via industrial tax reduction (O Huallachain, et al., 1992). The incentives to accelerate the region's economic growth can be provided by financial incentives for private investment such as tax reduction, land purchase subsidies, low-interest loans, and loan guarantees (Leitner, 1990). Some of the problems in Turkey are high emissions and low usage of renewable energy. Consequently, the Turkish government provides 4 types of incentives that are; reduction and elimination of license fees; priority of distribution connection; financial contribution in research and development (R&D) in environmental quality improvement and small and medium enterprises; and tax credit for R&D costs. The Turkish government also implements disincentives such as higher taxes for companies producing waste disposals (Kaya, et al., 2006). Radermacher and Brinkmann (2011) propose a micro insurance for the poor in developed countries. In dealing with marine pollution, certified ship or quality shipping can be used as an incentive to reduce naval pollution (Kaps, 2004). The United States government implements wage subsidy for companies that employ disabled workers (Warner and Polak, 1995). To reduce private vehicle use, the Bristol City Government provides road user charges as a disincentive mechanism (Jakobsson, et al., 2002). In order to reduce environmental degradation due to plastic bags, the Irish government provides disincentives by additional tax charges for the use of plastic bags (Sugii, 2008). To reduce the amount of solid waste, some

provinces in the United States use an incentive called Pay as You Throw (PAYT). The mechanism of this disincentive is that the community will be charged according to the weight of waste disposed of (USA Environmental Protection Agency, 2013). A complete overview of proposed instruments based on literature can be seen in Table 2.

Table 2. Proposed Instruments

| Group | Instruments | Literature |

|---|---|---|

| Zoning | 1) Re-zoning | Girling and Helpland, 2007 |

| 2) Special zone for particular activities | Girling and Helpland, 2007; O Huallachain and | |

| Sattertwaite, 1992 | ||

| Licensing | 3) Building permit | Government Regulation No. 15, 2010 concerning |

| 4) Permit for trading business | instruments for Provincial and Municipal in the | |

| 5) Permit for industrial enterprises | development control | |

| 6) Permit for tourism businesses | ||

| Sanction | 7) Warning | Government Regulation No. 15, 2010 concerning |

| 8) Written warning | instruments for Provincial and Municipal in the | |

| 9) Temporary suspension of activities | development control | |

| 10) Temporary suspension of public services | ||

| 11) Revocation of license | ||

| 12) Cancellation of license | ||

| 13) Site closing | ||

| 14) Imprisonment | ||

| 15) Civic sanctions | ||

| Incentives | 16) Providing job training | O Huallachain and Sattertwaite, 1992. |

| 17) Micro-insurance | Radermacher and Brinkmann, 2011. | |

| 18) Priority in infrastructure development | Patras, 1990; Leitner, 1990. | |

| 19) Awards | Milne and Bruss, 2008; Paula, et al. 2012. | |

| 20) Sponsorships | Fu et al., 2011. | |

| 21) Gifts | Fu et al., 2011. | |

| 22) Education priority | Kingma, 2003. | |

| 23) Funds allocation in environmental rehabilitation | Sugii, 2008. | |

| 24) Financial assistance for companies that employ disabled employees. | Warner and Polak, 1995; Tsai and Rosenheck, 2013. | |

| 25) Licensing incentives for company expansion | Fu et al., 2011. | |

| 26) Funding of tax increases | Thomas, 2001. | |

| 27) Reduction of income tax for 5 years | Zuluaga and Dyner, 2006; Lee, 2008. | |

| 28) Reduction of land rent tax | Wanhill, 1986. | |

| 29) Exemption of tax operations | Lee, 2008; Pappis, 1990; Zuluaga and Dyner, 2006; O Huallachain and Sattertwaite, 1992. | |

| 30) Subsidies the purchase of land | Leitner, 1990. | |

| 31) Insurance premium discount | Kousis, 1989; Radermacher and Brinkmann, 2011. | |

| 32) Reduction of profit tax revenue | Leitner, 1990; Pappis, 1990; O Huallachain and Sattertwaite, 1992; Zuluaga and Dyner, 2006; Lee, 2008. | |

| 33) 15-20 years guarantee no tax increases profit | Wanhill, 1986; Thomas, 2001. | |

| 34) Reduction of profit tax that has not been invested for 10 years | Wanhill, 1986. | |

| 35) Money grant to developers | Fu et al., 2011. | |

| 36) Funds allocation for small and medium | Kaya et al., 2008. | |

| businesses |

| Group | Instruments | Literature |

|---|---|---|

| Incentives | 38) Loan guarantee | Leitner, 1990; Zuluaga and Dyner, 2006. |

| 39) Incentives in land certification | Government Regulation No. 12/ 2012. | |

| 40) Tax exemption for R&D | Leitner, 1990; O Huallachain and Sattertwaite, | |

| 1992; Lee, 2008. | ||

| 41) Loan for paying R&D Tax | Zuluaga and Dyner, 2006. | |

| 42) Low interest for loans | Leitner, 1990. | |

| 43) Lower land prices than the competitors | Wanhill, 1986. | |

| 44) Discounts fees of traffic in all ports | Harte et al., 2007. | |

| 45) Harbor fees reduction | Harte et al., 2007. | |

| 46) Corporate income tax exemption | Lee, 2008. | |

| 47) Personal income tax exemption | Lee, 2008. | |

| 48) Certain types of fishing permits for | Kaps, 2004; Harte et al., 2007. | |

| fishing | ||

| 49) Allowing the producers to import | Lee, 2008. | |

| materials/inputs used for the production | ||

| of export products, without charging | ||

| excise | ||

| 50) Reduction/exemption of import duties | Lee, 2008. | |

| 51) Reduction and exemption license fee | Lee, 2008. | |

| Disincentives | 52) Restrictions on logging permits | Guillerme et al., 2011. |

| 53) High taxes polluted industry | Kaya et al., 2008. | |

| 54) Additional tax | Sugii, 2008. | |

| 55) Exemption of land taxes and capital. | Lee, 2008. | |

| 56) Charging of fees according to the | Kaya et al., 2008. | |

| weight of waste disposed | ||

| 57) Additional charges for purchases using | Sugii, 2008. | |

| plastic bags | ||

| 58) Electronic Road Pricing | Jakobsson et al., 2004. | |

| 59) Transferable development rights | Linkous, 2016. | |

| 60) Reduction of fish harvest quota allowed | Harte et al., 2007. |

Possible Adopted Development Control Instruments

60 proposed instruments were assessed in terms of the six criteria of public policy via questionnaires. This assessment identified the main objectives of all stakeholders in development control. The questionnaires also identified possible authorization of all possible adopted instruments in different government levels.

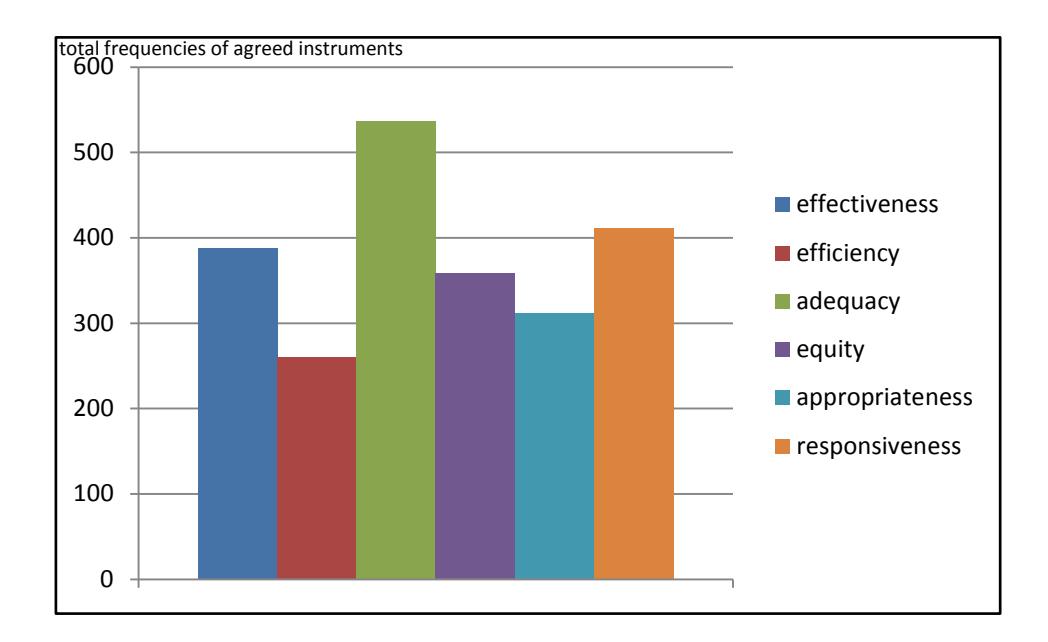

In terms of public policy, the proposed instruments have been valued as the adequacy criteria. It indicates that the coverage of development control is the first priority for the government to cope with development issues in GKS. Following adequacy, responsiveness and effectiveness are the second and third important criteria. Consequently, respondents emphasize that the development control in GKS should be more on effective response to all the issues with various alternatives. Figure 2 describes the output of questionnaire based on the public policy criteria.

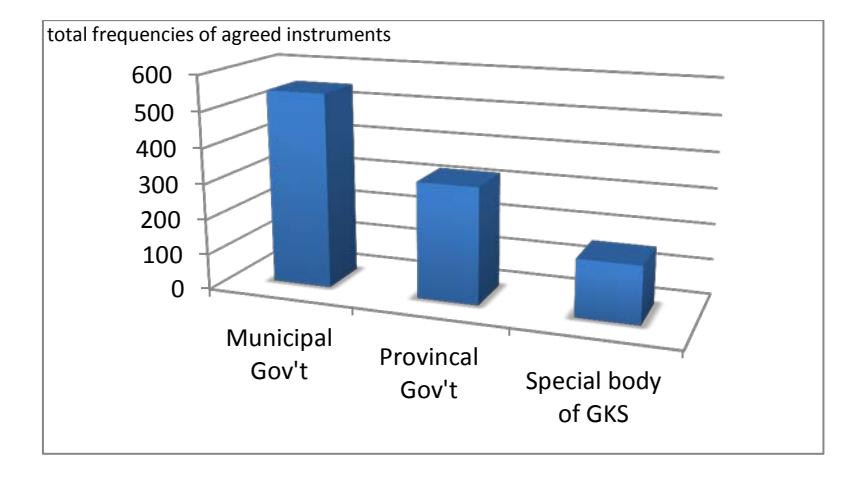

Based on the questionnaires, respondents approve of all proposed instruments in different ways. Most of the instruments are considered primarily as municipal authority. 7 of them are more on the level of provincial authority than on the level of the municipalities and GKS. Most of the instruments authorised by provincial levels are instruments about taxes, export-import, seaports and new mechanisms such as ERP (electronic road pricing). This conclusion is in line with the authority of central and provincial government levels under the Government Regulation No. 15 in 2010 concerning instruments for Provincial and Municipal governments in development control. Last but not least, none of them are considered dominantly as part of GKS authority. In sum, Figure 3 illustrates the distribution of the tallying process on possible instruments for development control among the three level of government. The municipal government has the highest number of tallying, indicating that most of the instruments are authorised by the municipal government. This is in line with autonomy regulation in Indonesia, which decentralised most authorities to the municipal level.

Figure. 2. Assessment result of development control instruments based on public policy criteria

Figure 3. Assessment result of GKS stakeholder's role from the questionnaire

Agreed Development Control Instruments

Having identified possible adopted instruments, the discussion is furthered into bridging commitment among government levels in implementing the instruments. FGD was selected since it can be used to discuss instruments in detail and can lead to an agreement on a particular instrument.

From the FGD, respondents have reduced the possible adopted instruments from 60 to 39 instruments (Table 3). Instruments such as import duties reduction, tax reduction, and income tax exemption are considered irrelevant since those instruments are identified under national

government authority. Strong agreements on particular instruments are usually related to the government authority arrangement under the Government Regulation No. 15 of 2010 concerning instruments for Provincial and Municipal in the development control. These instruments are in strong agreement including providing job training, re-zoning, micro insurance, priority in infrastructure development, and warnings. These instruments are relevant to overcome the spatial problems in GKS and are also under the municipal, provincial governments, and special body of GKS's authority.

Table 3. Instruments for development control in GKS

| Group | Instruments | ||

|---|---|---|---|

| Zoning | 1) Re-zoning | ||

| 2) Special zone for particular activities | |||

| Licencing | 1) Building permit | ||

| 2) Permit for trading business | |||

| 3) Permit for industrial enterprises | |||

| 4) Permit for tourism businesses | |||

| Sanctions | 1) Warning | 6) Cancellation of license | |

| 2) Written warning | 7) Site closing | ||

| 3) Temporary suspension of activities | 8) Imprisonment | ||

| 4) Temporary suspension of public services | 9) Civic sanctions | ||

| 5) Revocation of license | |||

| Incentives | 1) Providing job training | 11) Funds allocation for small and | |

| 2) Micro insurance | medium businesses | ||

| 3) Priority in infrastructure development | 12) Transferable development rights | ||

| 4) Awards | 13) Loan guarantee | ||

| 5) Sponsorships | 14) Incentives in land certification | ||

| 6) Gifts | 15) Tax exemption for R&D | ||

| 7) Education priority | 16) Loan for paying R&D Tax | ||

| 8) Funds allocation in environmental rehabilitation | 17) Low interest for loans | ||

| 9) Financial assistance for companies that employ | 18) Land purchasing | ||

| disabled employees. | 19) Insurance for low-small | ||

| 10) Licensing incentives for company expansion | businesses | ||

| Disincentives | 1) Restrictions on logging permits | 4) Electronic Road Pricing | |

| 2) High taxes polluted industry | 5) Transferable development rights | ||

| 3) Additional tax | |||

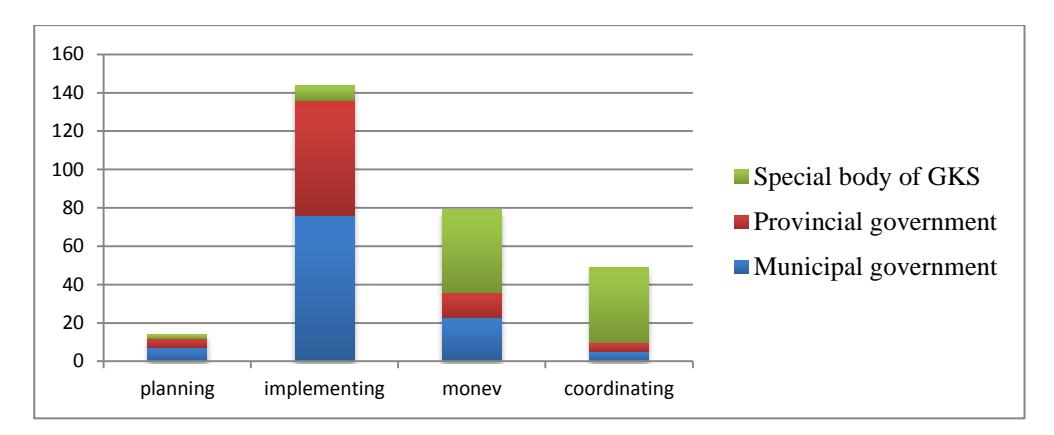

Figure 4. Roles of the three government levels in GKS development control

The 39 agreed instruments highlight the importance of authorization in every government level. Then, the authorization brings ideas for certain responsibilities for each of the level in managing GKS. To uncover those responsibilities, the FGD also discusses and makes the three

government levels' commitment in four stages of development that are planning, implementation, monitoring and evaluation (Monev) and coordination. The provincial and municipal levels are considered to have more responsibility in implementation rather than the other three stages. Interestingly, the GKS body will have greater responsibility in monev and coordination than the other three stages. Therefore, the body should be defined as a coordinating body rather than acting body. Figure 4 illustrates the role of every government level in each stage of development for GKS development control.

Implementing Development Control Instruments

In designing the implementation of development control instruments, we considered only the agreed instruments. Since the government has four groups of development control, we designed the application process for the agreed instruments into four sections, namely; zoning plan, incentives/disincentives, licensing and sanction. Since the main problem in KSN GKS is coordination among government levels, the application design for agreed instruments is focused on how the KSN GKS body, municipal, and provincial government levels can collaborate in implementing the instruments. To create the application design, we reviewed the output of the FGD, particularly on the agreed instruments. Moreover, we also reviewed stakeholders' key comments, difficulties, and challenges of the development process in GKS during the FGD. As a result, we propose four designs following the four groups of development control in implementing the agreed instruments.

Zoning Plan

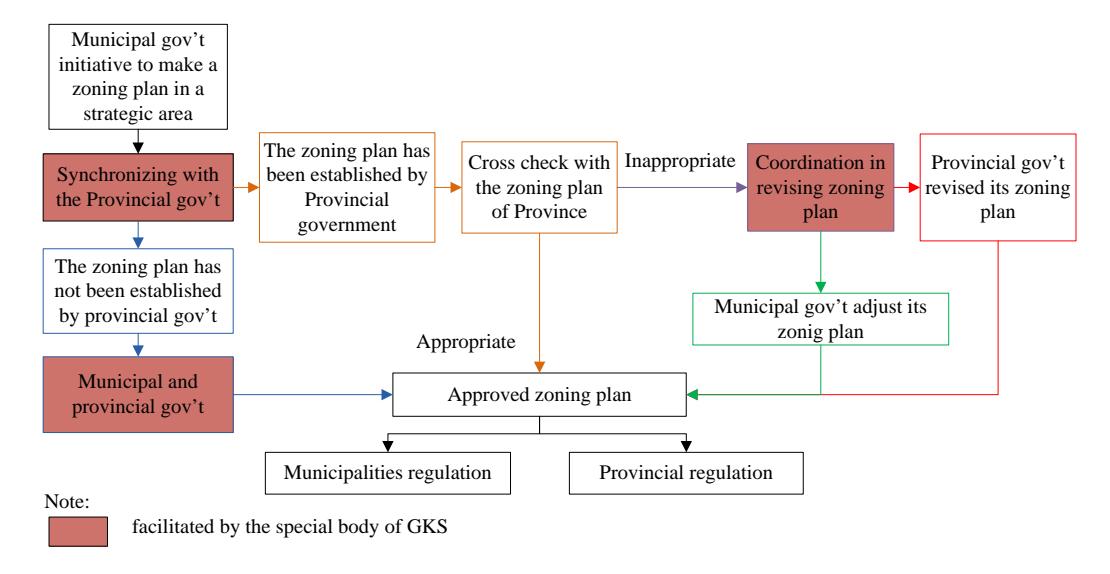

One of the agreed instruments is re-zoning in GKS special zones. In the re-zoning, the provincial and municipal government levels share similar roles in the four stages of development control. Specifically, the GKS authority will only have a coordinating function to synchronise both the provincial and municipal governments' interests. Consequently, the rezoning process should be arranged by combining all three authorities in terms of their roles and responsibilities.

Figure 5. Synchronization scheme of zoning plan formulation in strategic areas

To synchronise these roles and responsibilities, Figure 5 illustrates the mechanism for coordination in the re-zoning process. The initiatives for re-zoning can be from either provincial or municipal governments. In the case of municipal initiatives, the re-zoning should be consulted with the provincial government. If there is no zoning plan on the provincial level for the same location, the re-zoning can be a collaboration process between municipal and provincial governments under the facilitation of GKS. Otherwise, the cross-checking process can be done in two ways for both the current provincial zoning plan and the draft of municipal rezoning plan. The GKS can play its coordination roles to strengthen the process. Once the agreed re-zoning plan is established among the parties, the same product can be legalised under municipal and provincial regulations.

Incentives/Disincentives

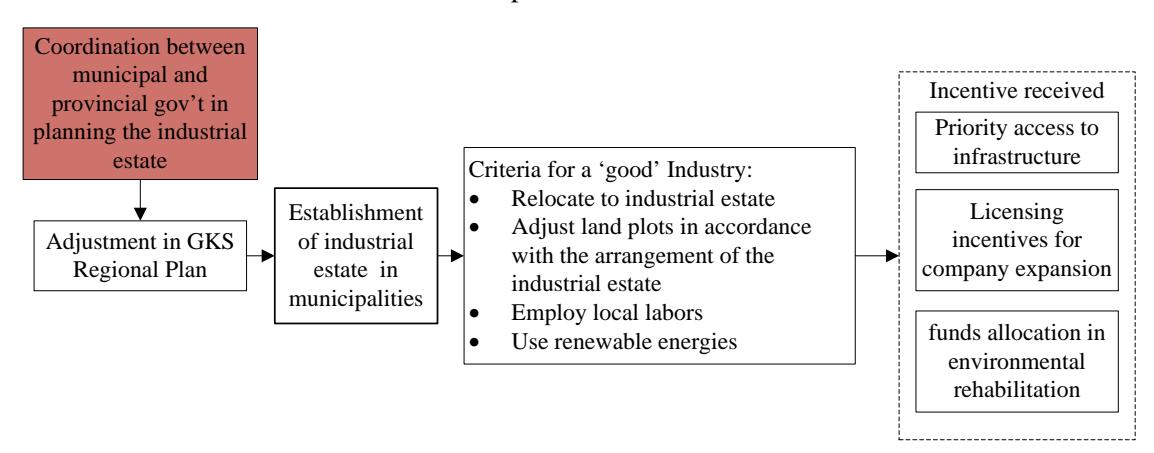

Development incentives/disincentives can be applied to the development of industrial estates. One of them is the industrial estate in Manyar, Gresik Municipality as one of the main programs in the GKS Regional Plan. The estate will accommodate existing industries in Gresik and incoming future investment. The estate concept can offer many benefits due to a prime location, availability of infrastructure, proximity to other related industry (agglomeration), and its segregation from other non-industry uses to minimise land use conflicts. It also provides an opportunity to improve facilities for maintaining environmental quality in a cost effective manner by allowing shared facilities such as common waste-treatment facilities (World Bank, 2012). The estate will also manage pollution from industries to the surrounding areas. Relocating industrial areas from urban centres and densely populated areas can improve ambient environmental quality in the areas (World Bank, 2012). Therefore, the economic and environmental values can be a win-win solution by providing a proper industrial estate. Industries which obey regulations and join the estate concept can be entitled to receive incentives from the government (Figure 6). The incentives could consist of priority access to infrastructure, licensing incentives for company expansion, and funds allocation in environmental rehabilitation. In terms of roles of the three government levels, the municipal and provincial governments will be responsible for providing incentives for any scheme mandatory by law. Furthermore, the GKS authority will play a coordinating role particularly in defining industrial estates across at least two municipalities in GKS.

Figure 6. Incentive scheme for any industry, which obeys regulation and joins the estate concept

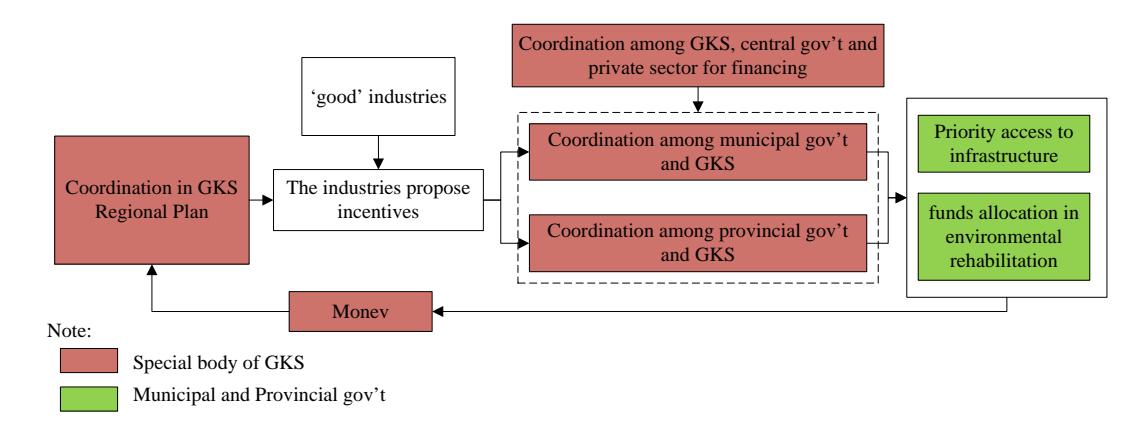

To have funds allocated for environmental rehabilitation and have priority in infrastructure development incentives, the coordination arrangement among the three government levels can be described as in Figure 7. The estate manager can propose these incentives to both the provincial and municipal governments. The GKS authority can verify the estate's roles, responsibilities, contributions and problems in the GKS Regional Plan. This verification can be one of the indicators to provide these incentives to the estate.

Figure 7. Incentive scheme on fund for environment rehabilitation and priority access to infrastructure

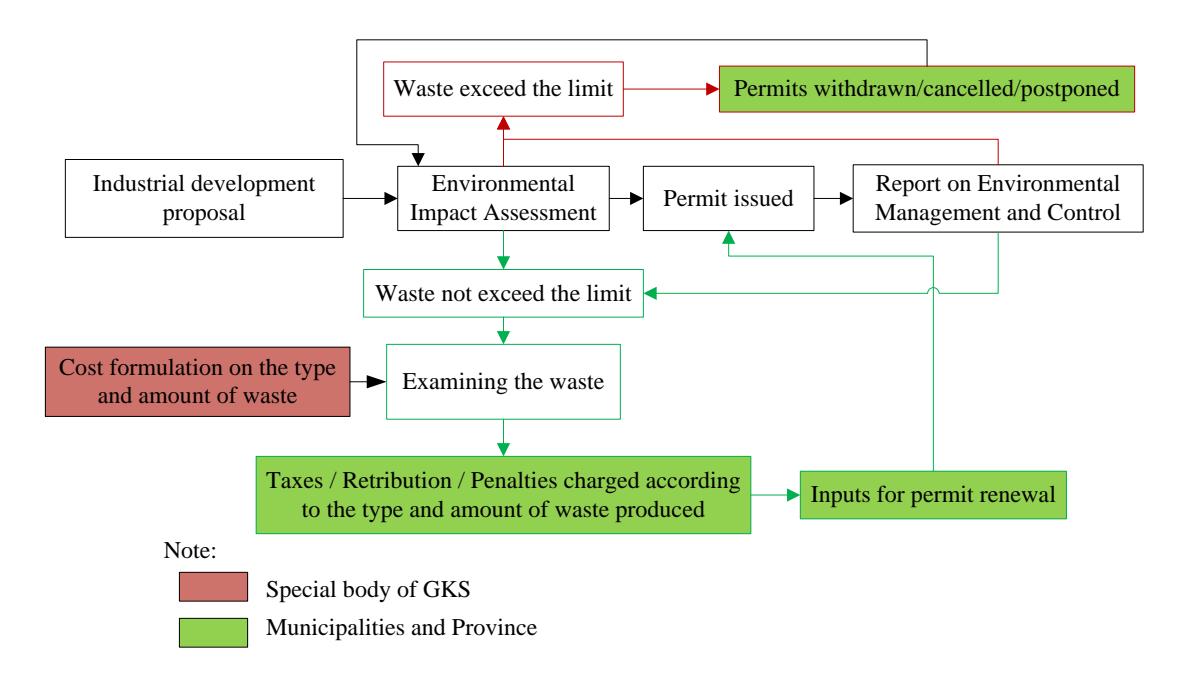

Figure 8. Disincentive schemes for industries

On the other hand, disincentive can be applied to industries with high pollution. For the national level, under the Environmental Ministry regulation No. 03/2010, the industrial waste should not exceed the waste water quality standard. This standard is also detailed by various Environmental Ministry regulations for each type of industry. To promote better environmental quality, the three levels of government can commit to applying more stringent regulations than the national level. This disincentive can be an additional cost for industries with additional pollution. In this case, municipal and provincial governments under the facilitation of the GKS body can

formulate the cost of additional pollution. The cost could be in the form of taxes, retribution or penalties. Therefore, the application of additional cost for polluting industry will minimize the level of pollution from industry activities as in Figure 8.

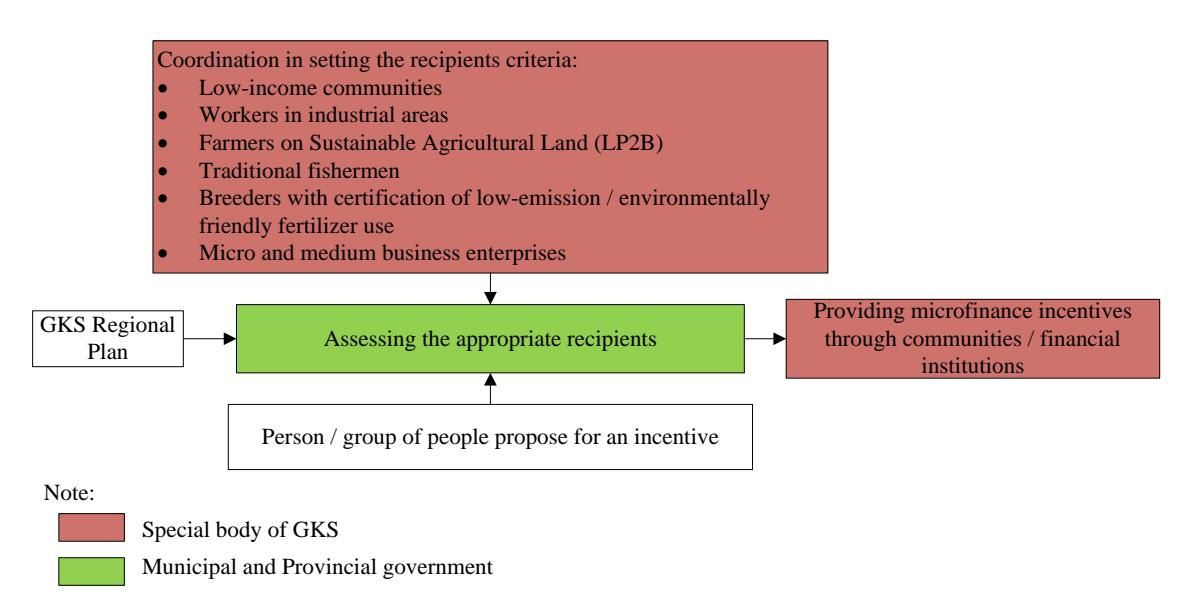

Microfinance incentives can also be part of a collaboration among the three levels of government. Providing insurance is part of the main programs in the GKS Regional Plan, 2010- 2030 such as the insurances for fire, harvest failure, farms, fishermen, small and medium business entrepreneurs, and health. Under the microfinance instruments, GKS can facilitate the municipal and provincial government in establishing criteria for beneficiaries. Having the criteria approved, the provincial and municipal governments can verify beneficiaries. Then, both levels of government can propose these beneficiaries to receive microfinance under GKS authority. Figure 9 illustrates the process from establishing the criteria until providing microfinance to the beneficiaries. Micro-insurance can be effective when it involves the community in distribution. Particular community groups that can cooperate with the GKS body in microfinance are koperasi, post offices, village offices, village credit institutions (e.g. LPD), and the East Java BPR (People Bank for Loan).

Figure 9. Disincentive schemes for microfinance

Licensing

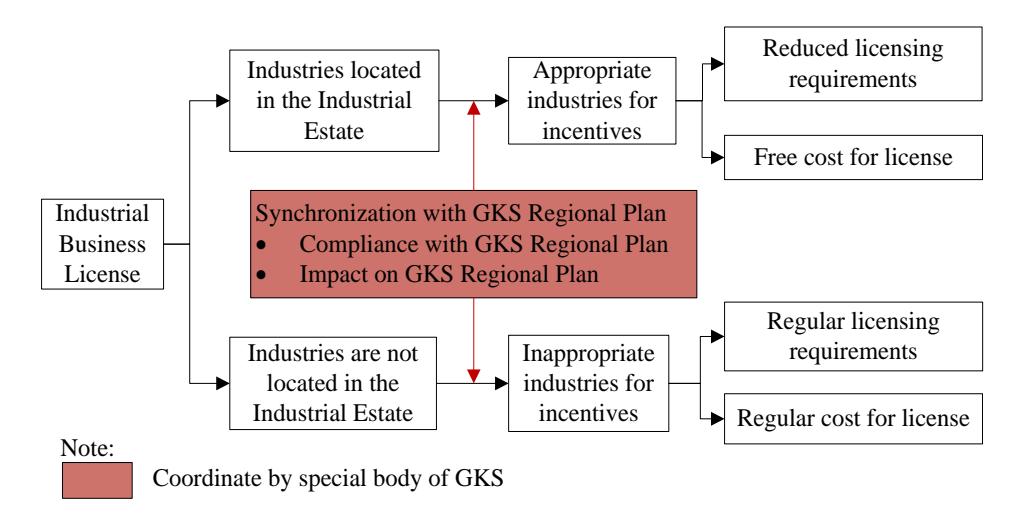

Licensing incentives for company expansion in GKS will not change the license regulations under both municipal and provincial authorities. The instruments are related to spatial use across two municipalities including industrial estates located in two municipal administrations. Figure 10 describes the process for licensing incentives for company expansion in industrial estates. GKS can play a role in selecting the company which complies with the GKS Regional Plan before municipal and provincial governments grant incentives to the company.

Figure 10. Licensing incentives for company expansion in industrial estates

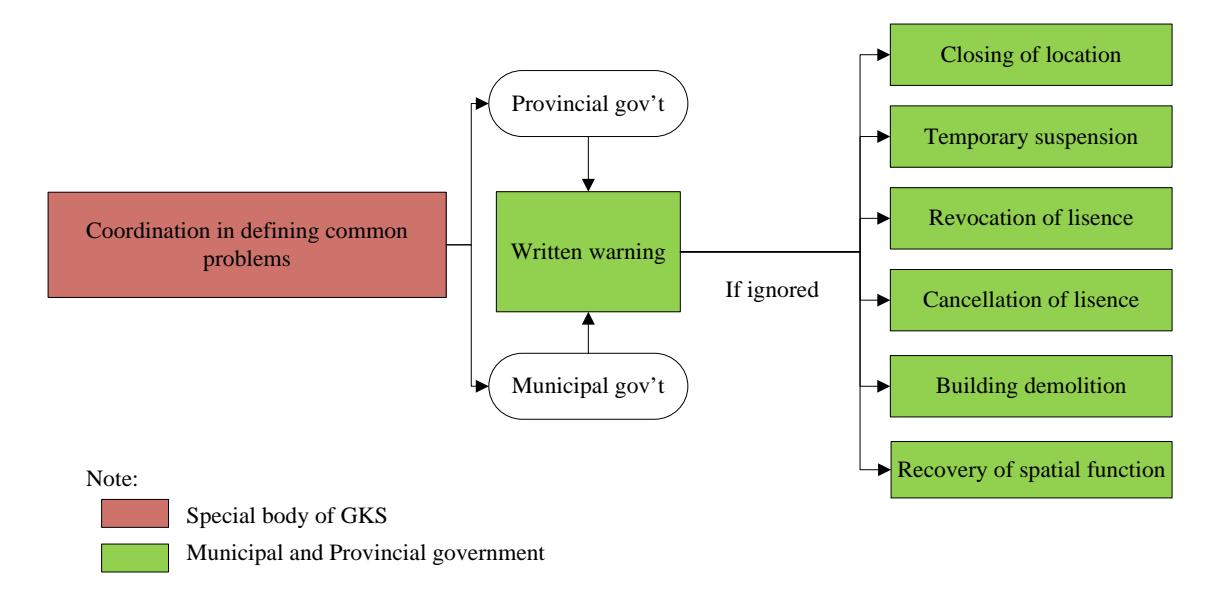

Sanctions

Under the sanctions-type of development control, GKS has a coordinating function for provincial and municipal governments before applying the instruments. The coordination process can only occur in cases involving more than one municipality and concern one of the GKS Plans. Those cases can be:

- 1. Agro-processing and fishery products development in Mojokerto and Sidoarjo

- 2. ERP development (Ecological Recycling Park) in Gresik, Surabaya, and Sidoarjo

- 3. Inter-City Water Supply Development (Water Supply Project of Umbulan & Water Supply Solo Project) which covers Gresik, Surabaya, Sidoarjo, Lamongan, and Pasuruan

Figure 11. Imposition of sanctions scheme under coordination of the GKS body

Figure 11 describes the implementation of the agreed instruments under sanction type of development control.

Conclusion

One of the key successes for the implementation of the GKS Regional Plan are the instruments for development control in GKS. The discussion among relevant stakeholders settled on 39 out of 60 instruments. These instruments consist of 2 instruments in zoning, 4 instruments in permits, 10 instruments in sanction, 17 instruments in development incentives and 5 instruments in development disincentives.

Based on the discussion, the GKS body will have a coordinating role to two other government levels. The coordinating function is a strategic role not only in the planning stage but also in the stages of implementation, monitoring, and evaluation. To avoid conflict among municipal and provincial government and the GKS body, the instruments are still following their original authorities based on the regulation. Therefore, the GKS body will not be viewed as the body which will take authorities from the other two government levels.

In particular for this location, which has at least two level administrative boundaries, the GKS body can carry out the function of coordination with the other two government levels. This function of coordination can be from the planning to the evaluation stage. This can also be applied to with a degree of importance for GKS areas. In addition, the function of coordination can also happen for the case that both levels of government at the moment have no relevant regulations/instruments established. The function of coordination can also be seen from the design of implementing development control instruments in the four groups of development control.