ABSTRAK

Dompet digital telah banyak diadopsi oleh masyarakat Indonesia dan memberikan peluang bagi industri fintech untuk berlomba menyediakan layanan yang terbaik bagi penggunanya. Meskipun layanan dompet digital cukup banyak diteliti, di berbagai belahan dunia, belum banyak yang memberikan gambaran komprehensif dan menyeluruh terkait profil dan karakteristik pengguna layanan dompet digital di Indonesia. Dengan demikian, penelitian ini bertujuan untuk mengetahui profil dan karakteristik masing-masing pengguna layanan dompet digital berdasarkan popularitasnya, yakni GoPay, OVO, Dana, LinkAja, dan ShopeePay. Selain itu, penelitian ini juga bertujuan untuk memahami perbedaan faktor demografi pengguna masing-masing layanan dompet digital. Dengan teknik metode analisis korespondensi berganda (MCA) pada data survei terhadap 409 pengguna layanan dompet digital di Indonesia, penelitian ini menghasilkan beberapa profil dan karakteristik pengguna yang berbeda. Selain itu, juga terbentuk beberapa klaster pengguna, yaitu pada analisis layanan dompet digital yang dimiliki oleh pengguna, hanya terbentuk tiga klaster, sedangkan untuk layanan dompet digital yang paling sering digunakan terdapat tujuh klaster. Temuan penelitian ini dapat membantu memahami profil dan karakteristik layanan dompet digital di Indonesia serta dapat digunakan sebagai informasi bagi para penyedia layanan dompet digital, baik dalam rangka meningkatkan kualitas layanan kepada penggunanya maupun menjangkau masyarakat yang lebih luas lagi.

Kata kunci: dompet digital, profil, karakteristik, MCA

INTRODUCTION

The development of technology has embraced all the aspects of life in society, including the economic aspect. Technological effects in the economic aspect can be seen in the payment process or transaction, which initially take the form of payment using physical money or cash, slowly being replaced by e-payment technology so that transactions can be cashless (Pramono, Yanuarti, Purusitawati, & Yosefin, 2006). E-payment has several types, including credit cards, e-wallets, e-money, online store value systems, digital accumulating balance systems, and wireless payment systems (Laudon & Traver, 2019). Of all these types of e-payments, e-wallet is the most frequently used payment method (Rapyd Research Study, 2020).

In Indonesia, there are various e-wallet service providers, ranging from bank and nonbank institutions, large companies, start-up companies up to the government also taking a part in this fintech industry. According to Bank of Indonesia (2020), there are 48 e-wallet service providers in Indonesia that have official licenses. Based on its popularity from Q4 2017 to Q2 of 2020 e-wallet players only fly around in the same name, those are GoPay, OVO, Dana, LinkAja and ShopeePay (Widiyanti, 2020; Devita, 2020). The five e-wallet providers compete for the first position.

GoPay is a product owned by PT Dompet Anak Bangsa which is a subsidiary of the startup company Go-Jek, PT Aplikasi Karya Anak Bangsa. At first, GoPay was only used to make payments on the Go-Jek application, an online transportation ordering service. This application is increasingly developing with various other services, also making Go-Pay more developed so that it can be used as a payment service with certain partners who work with Go-Jek. OVO is a product of the start-up company PT Visionet Internasional which is affiliated with the large company Lippo Group (Franedya, 2019). Unlike GoPay, which was born from Go-Jek, OVO stands independently as a company that focuses on its fintech and collaborates with other companies, such as Matahari Department Store, Tokopedia, Grab, and others (Widiastuti, 2018; Walfajri, 2019). Dana established since 2018 is managed by PT Espay Debit Indonesia with foreign investors from China, namely Ant Financial (AliPay) (Gumiwang, 2019). Like OVO, Dana stands independently as a e-wallet service, so that it has its own mobile application. LinkAja is the only government-owned e-wallet service through the Badan Usaha Milik Negara (BUMN) (Laucereno, 2019). LinkAja, formerly known as TCash, is a combination of several large companies, namely PT Telekomunikasi Seluler along with BUMN members, namely PT Bank Mandiri, PT Bank Negara Indonesia, PT Bank Rakyat Indonesia, PT Bank Tabungan Negara, PT Pertamina and PT Asuransi Jiwa Sraya (Rizaldi, 2020). Meanwhile, ShopeePay is a payment service on the e-commerce platform managed by SeaMoney Indonesia. The company is part of Shopee's parent Sea Group, Shopee (Annur, 2020). Shopee is an e-commerce platform focused on mobile applications based in Singapore.

According to Soegoto and Tampubolon (2020), e-wallet users in Indonesia are in the group of 20 to 30 years old at around 52.3%, followed by adolescents with less than 20 years old at around 33.3%. The remaining 13.3% is elderlies with an age of more than 40 years old. The age factor also has a significant influence on users of e-wallet services in Nigeria, the increasing age of a person, the lower the acceptance rate of e-wallet services (Akinbile, Akwiwu, & Alade, 2014). In Indonesia, there is relatively no differences in terms of e-wallet acceptance factors between ages, but for gender itself that female users are likely more influenced by the surrounding rather than male, and male reports higher scores than female about the risk of using e-wallet services (Saputri & Pratama, 2021b).

The acceptance factor of Dana e-wallet services in Indonesia is influenced by factors of trust, the lifestyle of its users, the influence of the surrounding environment and habits (Raihan dan Rachmawati, 2019). The acceptance factor of e-wallets in Java is influenced by performance expectations, perceived ease of use, the influence of the surrounding environment, security of services, user lifestyle, and relative benefits (Angelina & Rahadi, 2020). Meanwhile in Manado, the acceptance factors for GoPay, OVO and are influenced by the ease of using the service, the usefulness or benefits obtained, trust in the service and risk factors (Legi & Saerang, 2020). From these studies, there's a different characteristic of users who tend to choose which e-wallet services they want to use. Anggraeni & Pratama (2021a) report that Dana is much more popular among younger users and seems to be more appealing to the middle-class economy, whereas GoPay and OVO are much appealing to the middle to upper class economy.

From some of these studies, there is lack of discussion that reveals the overall profile and behaviour characteristics of e-wallet users in Indonesia. There is a lot of research concentrated on the acceptance factors of e-wallet services and still carried out in a limited location, because it simply focuses on some specific areas only.

in Indonesia. The data analysis technique used in this study was descriptive and inferential statistics. The analysis method used in this study is MCA (Multiple Correspondence Analysis).

METHOD

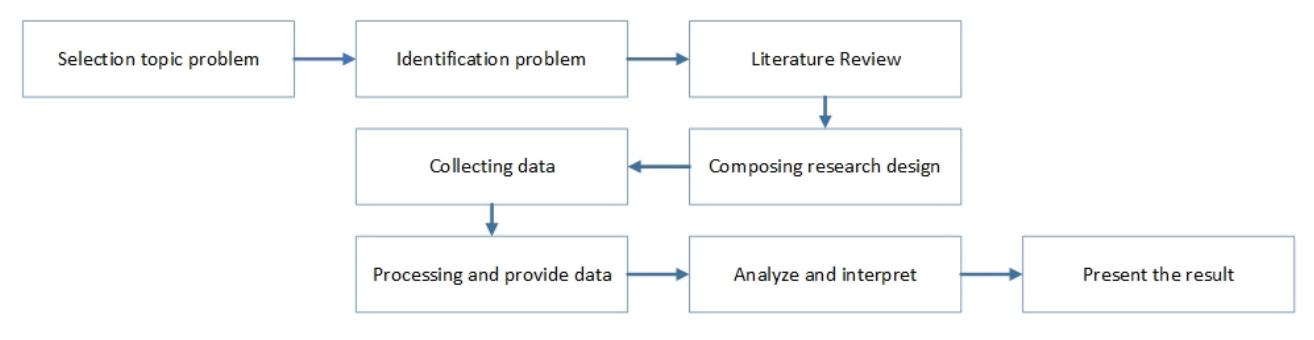

This research begins with the selection of issues to be discussed, that is the profile and characteristics of e-wallet users in Indonesia, i.e. GoPay, OVO, Dana, LinkAja and ShopeePay. This selection is based on the popularity of the top five e-wallet services in Indonesia (Widiyanti, 2020; Devita, 2020). After the selected topic has been set, the next step is to conduct a literature review to escalate the insight and as a reference in preparing research design. Afterwards, the collected data will be processed, analyzed and interpreted as primary data in this study. The next step is to present the findings as the result of the research. The detailed stages can be seen in Figure 1.

Figure 1 Problem Solving Stages

The lack of research raises the topic of the profile and characteristics of e-wallet users in Indonesia in order to find out how the profile and characteristics users of each e-wallet service in Indonesia and how the differences in age, sex, education level and demographic factors influence another, and therefore this study would do such an analysis of the profiles and characteristics of e-wallet users in Indonesia. The purpose of this study is to determine the profile and characteristics of e-wallet users in Indonesia based on the usage frequency, as well as to find out differences in age, sex, education levels and other demographic factors that can affect the usage frequency of e-wallet services

Data Collection Procedures

This study was designed to collect general demographic information, specifically age, sex, place of residence, place of origin, education, field of work, type of work and income. In addition, what kind of e-wallet services have been used and the usage frequency per week were collected. Primary data obtained through filling out online questionnaires independently then analyzed quantitatively using statistics on R software. Criteria for respondents from this study are residing in the territory of Indonesia, have used e-wallet services and are at least 17 years old. By using 95% Confidence Level (CL) and 5% Margin of Error (MoE), the required

sample data is at least 385 data. Data collection was carried out from March to August 2020 via Google Forms. 409 respondents participated in this study as summarized in Table I below.

Correspondence Analysis) analysis technique with the help of the several R packages, namely FactoMiner (Husson, Josse, Le & Mazet, 2020), Factoextra (Kassambara, 2020) and

TABLE I DEMOGRAPHIC INFORMATION OF ALL SAMPLES IN THIS STUDY

| Variable | Categories | Total (%) |

|---|---|---|

| Age | Less than 21 years old | 33 (8.07) |

| 21-25 years old | 255 (62.35) | |

| 26-30 years old | 85 (20.78) | |

| 31-35 years old | 14 (3.42) | |

| 36-40 years old | 11 (2.69) | |

| More than 40 years old | 11 (2.69) | |

| Sex | Male | 188 (45.97) |

| Female | 221 (54.03) | |

| Location | Sumatra | 20 (4.89) |

| Jawa | 334 (81.66) | |

| Bali dan Nusa Tenggara | 15 (3.67) | |

| Kalimantan | 24 (5.87) | |

| Sulawesi | 9 (2.20) | |

| Papua | 7 (1.71) | |

| Occupation | Unemployed | 37 (9.05) |

| Students | 33 (8.07) | |

| Government | 62 (15.16) | |

| ICT | 110 (26.89) | |

| Banking and Finance | 13 (3.18) | |

| Freelance | 31 (7.58) | |

| Others | 123 (30.07) | |

| Income | Low | 232 (56.72) |

| Middle | 161 (39.36) | |

| High | 16 (3.91) | |

| Education | No College Degree | 86 (21.03) |

| Undergraduate Degree | 305 (74.57) | |

| Postgraduate Degree | 18 (4.40) | |

| Total | 409 (100) | |

Data Analysis

This research is designed to collect general demographic information, e-wallet services usage and the usage frequency of these services. The data obtained were then analyzed statistically using R ver.3.6.2 on Rstudio. The data analysis technique in this study used the MCA (Multiple

FactoInvestigate (Thuleau & Husson, 2020). The result was carried out with the Hierarchial Clustering on Principle Components (HCPC) function with the default coefficient value = 1.

The MCA method was chosen as a method for analyzing and mapping the profiles and characteristics of e-wallet service users in Indonesia, namely GoPay, OVO, Dana, LinkAja and ShopeePay. In the MCA process, which is carried out to determine the profile and characteristic of the users of each e-wallet service, demographic data of respondents in the form of age, sex, location, education, occupation, and monthly income are used as supplementary variables. As active variables, the data of the e-wallet service and the usage frequency are used to map the usage patterns of each e-wallet service by the respondents.

RESULTS AND DISCUSSION Descriptive Statistics

Descriptive statistics was conducted to provide an overview of the survey data used in this study. The findings are obtained through descriptive analysis in the study presented in the following section.

less than Rp3,000,000.00 per month, middlerange income, which is Rp3,000,000.00 to Rp. 9,999,999.00 per month, and high income at Rp10,000,000.00 or more per month.

From the sample data of e-wallet service users in Indonesia, the majority of them are between 21 and 25 years of age, accounting for 62.35% of the total respondents. As many as 54.03% of the sample data were female. The majority of the sample data are located in Java, followed by Kalimantan, Sumatra, Bali and Nusa Tenggara, Sulawesi and lastly Papua. More than quarter of respondents work in the ICT (Information Communication Technology) sector (26.89%) followed by respondents who work at Government sector (15.16%). More than half of respondents have low income (56.72%) and an Undergraduate Degree (74.57%).

TABLE II TOP FIVE E-WALLET SERVICES IN INDONESIA

| Number of Users | Most Used by Users Total (%) | ||||

|---|---|---|---|---|---|

| E-wallet Services | Total (%) | ||||

| GoPay | 293 | (71.64) | 128 | (31.84) | |

| OVO | 267 | (65.28) | 164 | (40.80) | |

| Dana | 177 | (43.28) | 44 | (10.95) | |

| ShopeePay | 168 | (41.08) | 39 | (9.70) | |

| LinkAja | 146 | (35.70) | 27 | (6.72) | |

As previously mentioned, a total of 409 e-wallet users participated in this study. Table 1 provides demographic information, i.e., age, sex, location, occupation, income, and educational attainment. The age information is divided into six categories, i.e., less than 21 years old, 21 to 25 years old, 26 to 30 years old, 31 to 35 years old, 36 to 40 years old, and over 40 years old. Of the total 34 provinces in Indonesia, location was divided into six groups based on the island region of the province, i.e., Sumatra, Java, Bali and Nusa Tenggara, Kalimantan, Sulawesi, and Papua. The income information is categorized into three categories, i.e., low income, which is

Table II shows the number of users for each e-wallet service in Indonesia which is divided into two criteria, its total number of users (i.e., market share) and the number of users who use it the most (i.e., loyal customers). E-wallet services that are mostly owned by respondents are GoPay (71.64%), followed by OVO (65.28%), Dana (43.28%), ShopeePay (41.08%) and LinkAja (35.70%). Meanwhile, the most frequently used e-wallet services are OVO (40.80%), followed by GoPay (31.84%), Dana (10.95%), ShopeePay (9.70%) and the last is LinkAja (6.72%). Based on these two results, it shows that even though GoPay is owned by the most respondents, the most frequently used e-wallet service is OVO, which is the top choice of close to half of the total respondents. In other words, OVO users are more loyal than GoPay users. The order for the next three places is Dana (third), ShopeePay (fourth), and LinkAja (fifth). The order is consistent, either based on market share or loyal customers.

As shown in Table III, the majority of all e-wallet services users across all age groups use less than three times a week, except for those between 36 and 40 years of age where more than half of them use e-wallet service three to six times a week (54.55%) and those between 31 and 35 years of age who are equally split between using their e-wallet services less than three times

TABLE III DEMOGRAPHICS AND USAGE FREQUENCY OF E-WALLET SERVICES

| Usage Frequency (per week) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Demographic | Category | < 3 times (%) | 3-6 times (%) | > 6 times (%) | Total (%) | ||||

| Age | Less than 21 years old | 20 | (60.61) | 9 | (27.27) | 4 | (12.12) | 33 | (8.07) |

| 21-25 years old | 139 | (54.51) | 76 | (29.80) | 40 | (15.69) | 255 | (62.35) | |

| 26-30 years old | 39 | (45.88) | 30 | (35.29) | 16 | (18.82) | 85 | (20.78) | |

| 31-35 years old | 7 | (50.00) | 7 | (50.00) | 0 | (0.00) | 14 | (3.42) | |

| 36-40 years old | 4 | (36.36) | 6 | (54.55) | 1 | (9.09) | 11 | (2.69) | |

| More than 40 years old | 7 | (63.64) | 4 | (36.36) | 0 | (0.00) | 11 | (2.69) | |

| Sex | Male | 92 | (48.94) | 72 | (38.30) | 24 | (12.77) | 188 | (45.97) |

| Female | 124 | (56.11) | 60 | (27.15) | 37 | (16.74) | 221 | (54.03) | |

| Location | Sumatra | 10 | (50.00) | 8 | (40.00) | 2 | (10.00) | 20 | (4.89) |

| Jawa | 172 | (51.50) | 107 | (32.04) | 55 | (16.47) | 334 | (81.66) | |

| Bali and Nusa Tenggara | (40.00) | 9 | (60.00) | 0 | (0.00) | 15 | (3.67) | ||

| Kalimantan | 17 | (70.83) | 4 | (16.67) | 3 | (12.50) | 24 | (5.87) | |

| Sulawesi | 4 | (44.44) | 4 | (44.44) | 1 | (11.11) | 9 | (2.20) | |

| Papua | 7 | (100.0) | 0 | (0.00) | 0 | (0.00) | 7 | (1.71) | |

| Occupation | Unemployed | 22 | (59.46) | 12 | (32.43) | 3 | (8.11) | 37 | (9.05) |

| Students | 20 | (60.61) | 9 | (27.27) | 4 | (12.12) | 33 | (8.07) | |

| Government | 31 | (50.00) | 22 | (35.48) | 9 | (14.52) | 62 | (15.16) | |

| ICT | 46 | (41.82) | 41 | (37.27) | 23 | (20.91) | 110 | (26.89) | |

| Banking and Finance | 8 | (50.00) | 4 | (25.00) | 4 | (25.00) | 16 | (3.91) | |

| Freelance | 15 | (53.57) | 12 | (42.86) | 1 | (3.57) | 28 | (6.85) | |

| Others | 74 | (60.16) | 32 | (26.02) | 17 | (13.82) | 123 | (30.07) | |

| Income | Low | 144 | (62.07) | 70 | (30.17) | 18 | (7.76) | 232 | (56.72) |

| Middle | 67 | (41.61) | 58 | (36.02) | 36 | (22.36) | 161 | (39.36) | |

| High | 5 | (31.25) | 4 | (25.00) | 7 | (43.75) | 16 | (3.91) | |

| Education | No College Degree | 48 | (55.81) | 31 | (36.05) | 7 | (8.14) | 86 | (21.03) |

| Undergraduate Degree | 162 | (53.11) | 95 | (31.15) | 48 | (15.74) | 305 | (74.57) | |

| Postgraduate Degree | 6 | (33.33) | 6 | (33.33) | 6 | (33.33) | 18 | (4.40) | |

| Total | 216 | (52.81) | 132 | (32.27) | 61 | (14.91) | 409 | (100.00) | |

a week or between three and six times a week. In terms of their sex, males tend to use e-wallet services more frequently than females do. More than half of female respondents (56.11%) tend to use e-wallet less than three times a week, contrary to 48.94% males who do the same. Regarding their locations, more than half of respondents who live in Sumatra (50.00%), Java (51.50%) and Kalimantan (70.83%) use e-wallet less than three times a week, even all of respondents who live in Papua (100.00%). On the other hand, most respondents who live in Bali and Nusa Tenggara use e-wallet service three to six times a week (60.00%) followed by less than three times per week of usage (40.00%). Students tend to use e-wallet less than three times a week (60.61%), which is the highest rate compared to any other occupations. Meanwhile, e-wallet users working in the ICT sectors tend to have the best distribution of e-wallet usage frequency as they are the only group where only less than half of them use their e-wallet services less than three times a week. Unsurprisingly, income has the most notable pattern when it comes to its relationship with e-wallet usage frequency. As the income goes up, so does the frequency of e-wallet usage. The highest rate of those with less than three times of usage frequency per week is the highest among the low-income group (62.07%) and the same is true for those who use their e-wallet three to times a week and the middle-income group (36.02%) or for those who use more than six times a week and the highincome group (43.75%). A similar but weaker association is shown by educational attainment. Users with a higher educational attainment tend to use their e-wallet services more frequently. Those without a college degree or with only an undergraduate degree mostly use their e-wallets less than three times a week at 55.81% and 53.11% respectively. Meanwhile, those with a postgraduate degree are equally split between the three categories of e-wallet usage frequency.

Used E-wallet Services

As explained earlier, the first MCA analysis involved all e-wallet services used by respondents, it means that a respondent could

mention more than one e-wallet services. Apart from all e-wallet services are owned, the usage frequency of e-wallet by respondents is also used as supplementary variables with demographic active variables.

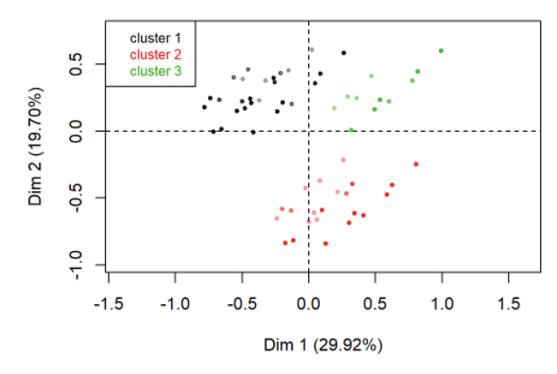

The results of the MCA analysis of the supplementary variables and active variables delivered 3 clusters as can be seen in Figure 2 and Table IV. Using the Diffusion of Innovation theory (Katz, Levin & Hertbert, 1963), each of clusters can represent an existing category, that is the Early Adopter category represented by the 1C cluster, the Early-Late Majority category is represented by cluster 1B and the Laggards is represented by cluster 1A.

Figure 2 Ascending Hierarchical of Individuals Based on the E-wallet Services They Used

The first cluster is 1A, this cluster fits the Laggards category where individuals in this cluster are reluctant to adopt e-wallet services. As can be seen in Table 4, this cluster is filled with individuals who barely used any e-wallet service. Looking at their demographics, most individuals in this cluster tend to have low income and are in Papua region. Only a small number of individuals in this cluster have middle-range income or work in Information and Communication Technology sector. Based on their e-wallet usage frequency, most individuals in this cluster use e-wallet sparingly i.e., only once or twice a week. Just a small number of individuals in this cluster use their e-wallet three times or more in a week.

The second cluster, 1B, is a good representation of the Early and Late Majority category because individuals in the cluster are more careful in adopting new innovations, so they only prioritize the two most popular e-wallet services, i.e., OVO and GoPay. This cluster consists of mostly individuals who live in Bali and Nusa Tenggara regions. Looking at their e-wallet usage frequency, most individuals in this cluster use e-wallet three to six times a week. Only a few individuals in this cluster use less or more a week.

The last cluster, 1C, is where the Early Adopters who are brave, enthusiastic, and ready to try new innovations before anyone else . All five e-wallet services tend to be adopted at the same time by individuals in this cluster. Most individuals in this cluster have middle or high income background. Only a few individuals who have low income and have no college degree belong to this cluster. Most of them use e-wallet more than six times a week. Only a few of them use their e-wallet less than that.

Most Frequently Used E-wallet Services

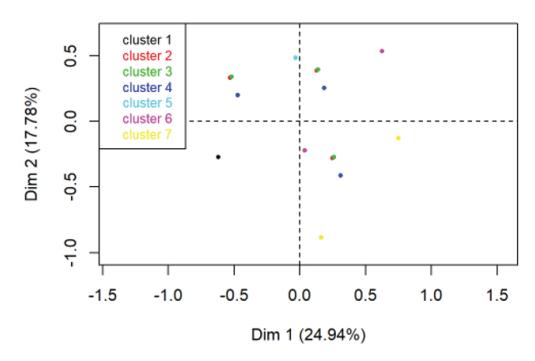

Table 2 shows that the most frequently used e-wallet service by respondents is OVO, as far as more than 40%, followed by GoPay, Dana, Shopeepay and the last is LinkAja. Based on the classification results using MCA, with each e-wallet service that is mostly used and the usage frequency as supplementary variables, 7 clusters of e-wallet service users in Indonesia were found as shown in Figure 3 and Table V.

The first cluster is 2A, containing individuals who are loyal to GoPay albeit with only less than three times per week of usage. This cluster is mostly dominated by female individuals. Only a few males and individuals who live in Bali and Nusa Tenggara belong to this cluster.

TABLE IV SUMMARY OF MCA ANALYSIS OF USED E-WALLET SERVICES

| Cluster E-wallet Services | Weekly Usage Frequency | Demographic | ||||

|---|---|---|---|---|---|---|

| 1A | (+) | (+) | Less than three times | Have low income Location: Papua | ||

| (-) | OVO GoPay LinkAja Dana ShopeePay | (-) | Three to six times More than six times | (-) | Have middle income Working at Information Communication Technology | |

| 1B | (+) | OVO GoPay | (+) | Three to six times (+) | Location: Bali and Nusa Tenggara | |

| (-) | (-) | Less than three times More than six times | (-) | |||

| 1C | (+) | OVO Dana LinkAja GoPay ShopeePay | (+) | More than six times (+) | Middle or high income | |

| (-) | (-) | Less than three times Three to six times | (-) | Have low income No college degree | ||

Notes: (+) most common characteristics

(-) least common characteristics

Figure 3 Ascending Hierarchical of Individuals based on the Most Frequently Used E-wallet Services

The second cluster, 2B, contains individuals who are loyal to LinkAja. This cluster is mostly dominated by individuals working in Banking and Finance sector.

The third cluster, 2C, contains individuals who are loyal to ShopeePay. There is nothing specific from their demographic information that characterize most individuals in this cluster. However, only a few individuals working in ICT sector belong to this cluster.

TABLE V SUMMARY OF MCA ANALYSIS OF MOST USED E-WALLET SERVICES

| E-wallet Cluster Services | Weekly Usage Frequency | Demographic | |||||

|---|---|---|---|---|---|---|---|

| 2A | (+) | GoPay | (+) | Less than three times | (+) | Female | |

| (-) | OVO Dana ShopeePay LinkAja | (-) | Three to six times More than six times | (-) | Male Location: Bali dan Nusa Tenggara | ||

| 2B | (+) | LinkAja | (+) | (+) | Working in Banking & Finance | ||

| (-) | OVO GoPay Dana | (-) | (-) | ||||

| 2C | (+) | ShopeePay | (+) | (+) | |||

| (-) | OVO GoPay Dana | (-) | (-) | Working in Information Communication Technology | |||

| 2D | (+) | Dana | (+) | (+) | Location: Bali and Nusa Tenggara Have low income Male Work on Freelance sector | ||

| (-) | OVO GoPay ShopeePay LinkAja | (-) | (-) | Female Postgraduate Degree Have middle income | |||

| 2E | (+) | OVO | (+) | Less than six times | (+) | Have low income | |

| (-) | GoPay Dana ShopeePay LinkAja | (-) | Three to six times More than six times | (-) | Postgraduate Degree Have middle income | ||

| 2F | (+) | OVO | (+) | More than six times | (+) | Have middle or high income Work at Information Communication Technology | |

| (-) | Dana ShopeePay LinkAja | (-) | Less than three times Three to six times | (-) | Have low income | ||

Notes: (+) most common characteristics

(-) least common characteristics

The 2D cluster contains individuals who are loyal to Dana. This cluster is mostly dominated by individuals who live in Bali and Nusa Tenggara, individuals who have low income, male individuals, or individuals working as freelancers. On the contrary, this cluster does not have many female individuals or individuals who have middle-range income.

The 2E cluster contains individuals who are loyal to OVO but with a low usage frequency, i.e., less than three times a week. This cluster consists of mostly low-income individuals. Only a few individuals with a Postgraduate Degree or who have middle-range income are in this cluster.

The 2F cluster contains individuals who are loyal to OVO with a high usage frequency, i.e., more than six times a week. This cluster is dominated by high and middle income individuals or those working in the ICT sector.

Finally, the last cluster, 2G, also contains individuals who are loyal to OVO with moderate usage frequency, i.e., three to six times a week. The cluster is dominated by middle-income individuals between 31-35 years of age.

CONCLUSION

Based on the results from data analysis of 409 e-wallet users in Indonesia in this study, some key findings on the profiles and characteristics of e-wallet service users in Indonesia were uncovered. First, while GoPay has the largest market share among any other e-wallet services in Indonesia, it is not the most frequently used e-wallet in Indonesia as the crown went to OVO, instead. In addition, this study also found that more than half respondents who use e-wallet services in Indonesia use the service no more than three times a week.

The results from classification analysis using MCA reveals three clusters of e-wallet users based on the adoption of e-wallet service, each representing early adopters who use all five of them (1C), early and late majorities who use the top two e-wallet services only (1B), and the laggards who barely use any e-wallet sevice at all (1A). Meanwhile, the same MCA also reveals seven different clusters of e-wallet users based on their most frequently used e-wallet service, each one representing loyal customer of GoPay (2A), LinkAja (2B), ShopeePay (2C), Dana (2D), and three clusters of loyal customers of OVO, one for each different usage frequency, i.e., low frequency (2E), high frequency (2F), and moderate frequency (2G). Each cluster has unique characteristics of users based on their demographic information, i.e., age, sex, location, occupation, income, and educational attainment.

The findings from this study can help to understand the profile and characteristics of e-wallet services in Indonesia, so that they can be used as inputs for all e-wallet service providers in Indonesia, both to improve their service quality to users and to reach a wider community. Increasing the quality of e-wallet services needs to be done because if a new technology is faced by rejections or low user acceptance rate, the technology will be abandoned because it cannot stand against other technologies or even the other competitors harnessing the same technology.

One limitation of this study has something to do with the distribution of sample that is, unfortunately, still heavily Java-centric. As such, this research can be further improved by having a more balanced respondents across all regions in Indonesia. Doing so can help confirm if the results from this study are, indeed, robust.

REFERENCES

Akinbile, L. A., Akwiwu, U. N. & Alade, O. O. (2014). Determinants of Farmers' Willingness to Utilie E-wallet for Accessing Agricultural Information in Osun State, Nigeria. Nigerian Journal of Rural Sociology, Vol. 15, No. 1, 105-113.

Angelina, C. & Rahadi, R. A. (2020). A Conceptual Study on The FactorsInfluencing Usage Intention of E-wallets in Java, Indonesia. nternational Journal of Accounting, Finance and Business, Vol. 5, No.27, 19- 29.

Annur, C. M. (2020). Strategi ShopeePay untuk Geser Dominasi GoPay dan OVO. Retrieved from: https://katadata.co.id/ desysetyowati/digital/5f4362f86c513/ strategi-shopeepay-untuk-geser-dominasigopay-dan-ovo

- Bank Indonesia, (2020). Informasi Perizinan Penyelenggara dan Pendukung Jasa Sistem Pembayaran. Retrieved from: https://www. bi.go.id/id/sistem-pembayaran/informasiperizinan/uang-elektronik/penyelenggaraberizin/Contents/Default.aspx

- Devita, V. D. (2020). E-Wallet Lokal Masih Mendominasi Q2 2019-2020. Retrieved from: https://iprice.co.id/trend/insights/ top-e-wallet-di-indonesia-2020/

- Franedya, R. (2019). Ini Deretan Investor Asing di Balik OVO & GoPay. Retrieved from: https://www.cnbcindonesia.com/ tech/20190211133328-37-54802/inideretan-investor-asing-di-balik-ovogopay

- Gumiwang, R. (2019). Geliat DANA di Bawah Dominasi GoPay dan OVO. Retrieved from: https://tirto.id/geliat-dana-dibawah-dominasi-gopay-dan-ovo-egmo

- Husson, F., Josse, J., Le, S. & Mazet, J. (2020). Multivariate Exploratory Data Analysis and Data Mining. Retrieved from: https://cran.r-project.org/web/packages/ FactoMineR/FactoMineR.pdf

- Kassambara, A. (2020). Extract and Visualize the Result of Multivariate Data Analyses. Retrieved from: https://cran.r-project.org/ web/packages/factoextra/factoextra.pdf

- Katz, E., Levin, M. L., & Hertbert H. (1963). Traditions of Research on The Diffusion of Innovation, American Sociological Review, 372-252.

- Laucereno, S. F. (2019). BUMN Bikin Perusahaan Pesaing GoPay dan OVO. Retrieved from: https://finance.detik. com/moneter/d-4427436/bumn-bikinperusahaan-pesaing-gopay-dan-ovo

- Laudon, K. & Traver, C. (2019). E-commerce 14th Edition, Business, Technology, Society. United States of America: Pearson Education.

- Legi, D., & Saerang, R. T. (2020). The Analysis of Technology Acceptance Model (TAM) on Intention to Use E-money in Manado (Study on GoPay, OVO, Dana), Jurnal Riset Ekonomi, Manajemen, Bisnis dan Akuntansi, Vol. 8, No.5, 624-632.

- Pramono, B., Yanuarti, T., Purusitawati, P. D., & Yosefin, T. E. (2006). Dampak Pembayaran Non Tunai Terhadap Perekonomian dan Kebijakan Moneter. Working Paper.

- Raihan, T., & Rachmawati, I. (2019). Analyzing Factors Influencing Continuance Intention of E-wallet Adoption Using UTAUT 2 Model (A Case Study of Dana Indonesia), e-Proceeding of Management, Vol. 6, No. 2, 1-8.

- Rapyd Research Study. (2020). Asia Pacific e-Commerce and Payments Guide 2020: India, Indonesia, Japan, Malaysia, Singapore, Soth Korea, Taiwan, and Thailand.

- Rizaldi, A. & Faruqi, F. A. (2020). Electronic Wallet as a Payment Transaction Instrument. IOP Conf. Series: Materials Science and Engineering 879, 1-7.

- Saputri, A. D., & Pratama, A. R. (2021a). Identifying User Characteristic of The Top Three E-wallet Services in Indonesia. IOP Conference Series: Materials Science and Engineering, 1-11.

- Saputri, A. D., & Pratama, A. R. (2021b). Perbandingan Sikap dan Penerimaan Pengguna Layanan Dompet Digital di Indonesia. Jurnal KomtekInfo, 154-162.

- Soegoto, D. S. & Tampubolon, M. P. (2020). E-Wallet as a Payment Instrument in the Millennial Era. IOP Conf. Series: Materials Science and Engineering 879, 1-7.

- Thuleau, F. & Husson, F. (2020). Automatic Description of Factorial Analysis. Retrieved from: https://cran.r-project. org/web/packages/FactoInvestigate/ FactoInvestigate.pdf

- Walfajri, M. & Kartika, H. (2019). Bermitra dengan Tokopedia, jumlah Pengguna OVO Naik Lebih dari 400%. Retrieved from: https://keuangan.kontan.co.id/ news/bermitra-dengan-tokopedia-jumlahpengguna-ovo-naik-lebih-dari-400

- Widiastuti, D. A. (2018). OVO Jalin Kerjasama dengan 4 Perusahaan, Grab Salah Satunya. Retrieved from: https://www. tek.id/tek/ovo-jalin-kerja-sama-dengan-4-perusahaan-grab-salah-satunyab1U2p9bND

- Widiyanti, W. (2020). Pengaruh Kemanfaatan, Kemudahan Penggunaan dan Promosi Terhadap Keputusan Penggunaan E-wallet OVO di Depok. Moneter: Jurnal Akuntansi dan Keuangan, 54-63.