Keywords:

demographic, geographical, TAM, Shopee Paylater, Solo society

The demographic and geographical conditions of the community are thought to have an influence on technology acceptance. However, there are not many studies which have evaluated the demographic and geographical conditions of the community in terms of the use of technology, especially application-based technology that directly interacts with the community. This study uses a modified technology acceptance model (TAM) as a theoretical framework. This case study investigates whether community demographics and geography influence the acceptance of Shopee Paylater among the people of Solo Raya. The model was validated using a questionnaire obtained from an online survey in the former Surakarta Residency as a representative for the people of Solo Raya. The results show that demographic conditions such as gender, age, and income and geographical conditions of residence have no significant influence on the technology acceptance model (TAM), which means demographic and geographical differences have no impact on the acceptance of technology within Solo society, especially the Shopee Paylater application. It is because there are no differences in access to technology or income levels in the Solo Raya. This research also shows that in a society that is relatively modern and has access to adequate infrastructure, it tends to be adaptive to new technology.

INFO ARTIKEL

ABSTRAK

Kata kunci:

demografi, geografi, TAM, Shopee Paylater, masyarakat Solo

Kondisi demografi dan geografi masyarakat diduga memiliki pengaruh dalam penerimaan teknologi. Namun, belum banyak penelitian yang mengevaluasi kondisi demografi dan geografi masyarakat pada penggunaan teknologi, khususnya teknologi berbasis aplikasi yang bersinggungan langsung dengan masyarakat. Penelitian ini menggunakan modifikasi technology acceptance model (TAM) sebagai kerangka teori. Penelitian studi kasus ini menyelidiki apakah faktor demografi dan masyarakat memengaruhi penerimaan Shopee Paylater pada masyarakat Solo Raya? Model tersebut divalidasi menggunakan kuesioner yang diperoleh melalui survei online di eks Karesidenan Surakarta sebagai representatif masyarakat Solo Raya. Hasil penelitian menunjukkan kondisi demografi seperti jenis kelamin, usia, dan pendapatan dan kondisi geografi tempat tinggal tidak berpengaruh secara signifikan terhadap technology acceptance model (TAM). Hal ini berarti tidak ada perbedaan masyarakat Solo Raya dalam menerima penggunaan teknologi, khususnya aplikasi Shopee Paylater. Dalam hal ini tidak ada perbedaan akses teknologi dan tingkat pendapatan pada masyarakat Solo Raya. Masyarakat yang relatif modern dan memiliki akses serta infrastruktur yang memadai cenderung adaptif terhadap teknologi baru.

Introduction

The economic dimension experiences technological impacts in payment procedures or transactions, transitioning from traditional physical currency or cash to gradually adopting e-payment technology (Saputri & R. Pratama, 2021). Financial technology, commonly known as Fintech, is a combination of information technology and financial services that has the ability to transform business models and provide convenience in entering the industry (Ilman, Nurjihadi, & Noviskandariani, 2019). Fintech is also defined as technological innovation in financial services that can generate business models, applications, processes, or products with material effects related to the provision of financial services (Nizar, 2020). In fact, according to Mention (2019), fintech is a financial service supported by innovative technology and accompanying business models. This phenomenon has led business players to continue innovating in the utilization of fintech. One popular form of fintech that has seen an increasing trend and has become one of the most popular payment options is PayLater (Adirinekso, 2021). PayLater has quickly gained penetration and has shown significant interest from users, and those who have not yet utilized PayLater have plans to use it in the future (Agadhita & Tjhin, 2023).

Various digital wallet applications are available in Indonesia, including ShopeePay, GoPay, LinkAja, Dana, and Ovo (Saputri, 2022), which collaborate with hundreds of thousands of online and offline merchants. Shopee offers various electronic payment options, such as bank transfers, credit cards, and the Shopee Paylater feature. Shopee Paylater is a loan product available on Shopee, where Shopee collaborates with other fintech lenders. As an e-commerce platform, Shopee provides services to fintech lenders to finance users who need financial assistance in the form of a balance to shop on Shopee (Setyawati, 2022).

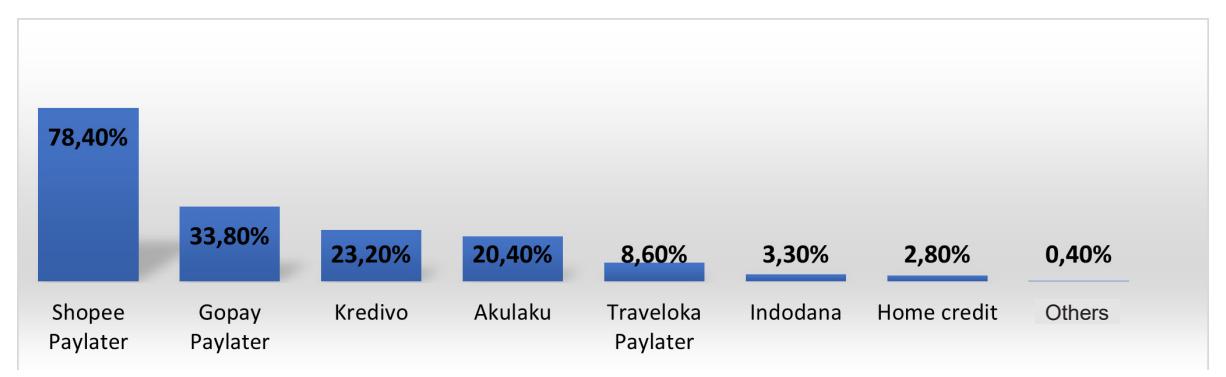

Figure 1 Paylater User Diagram in 2021 Source: Daily Social, 2023

According to Fintech 2021, reported by Daily Social, Shopee Paylater is the most widely used Paylater service in Indonesia, with 78.4% of the 1,500 respondents using the application. According to Ratu et al. (2019), interest in usage is defined as the level of someone's strong desire or motivation to take a specific action in using an application. After consumers have a positive experience using an application, there is an interest when using it again. In its usage, users consider various factors to achieve efficiency and effectiveness. According to Auralia, Manggabarani, & Wahyudi (2022), there are several indicators to identify repurchase intention, including: transactional interest, which is an individual's desire to reuse a product they have used before; referential interest, which is an individual's willingness to recommend a product they have used to others; preferential interest, which is an individual's attitude that prioritizes a specific product and can only be replaced if there are issues with the preferred product; and exploratory interest, which is an individual's attitude of seeking further information about a product and aiming to uncover the positive value of the technology product being used.

There is an assumption that technological development follows the process of technology dissemination from urban to rural areas. Research on the influence of geography on technology adoption is still limited. It is worth noting that urban areas are considered the center of technological development, while rural areas may lag in technology adoption, leading to potential delays. Apart from geographical differences, demographic variations also influence technology usage. According to a study by Ratu et al. (2019), there is a correlation between socio-demographic factors and the use of technology based on social media in businesses. On the other hand, research by Husein (2017) suggests that demographic characteristics do not moderate perceived technological benefits and implementation risks in relation to the intention to use an application. Thus, this study examines whether demographic and geographic conditions serve as control variables in the model of technology reuse intention. Andika & Rastini (2013) mention four demographic variables that can influence consumer technology usage, including age, gender, education, and income. As for the geographical aspect, according to Grace, Tanciga, & Nurdin (2018), geographical location refers to the position of a region based on its location and shape on the Earth's surface. Geographical location is usually defined by various geographic features and place names. In the context of this study, geographical conditions refer to the residential location of individuals based on rural or urban boundaries.

Several models have been constructed to analyze and understand the factors that influence the acceptance or usage of technology. These models include the Theory of Reasoned Action (TRA), the Theory of Planned Behavior (TPB), and the Technology Acceptance Model (TAM), developed by Fred D. Davis in 1989. Venkatesh and Davis (2000) stated that TAM is a fairly good concept, as it can explain 40% of the behavior and usage intensity towards new information technology systems. Therefore, TAM is one of the most popular and widely used models in research on technology usage because of its simplicity and ease of application. Consequently, this study utilizes TAM to develop the conceptual framework for the research (Siregar et al., 2022). Davis (1989) explained that the Technology Acceptance Model (TAM) is a model that can predict and explain how users accept and use technology related to their job by examining the constructs of perceived usefulness and perceived ease of use, as well as the adoption risk of the software being used.

Based on research conducted by Putri and Iriani (2020), Priskilia and Sitinjak (2019) and Canestren and Saputri (2021). It is stated that perceived ease of use has a positive and significant impact on the intention to reuse technology. However, on the other hand, research conducted by Asja, Susanti, and Fauzi (2021) showed that perceived ease of use does not have a significant impact on the intention to reuse technology. Perceived ease of use is defined as the extent to which an individual believes that using a technology will be free of effort. This factor will eventually impact behavior, whereby the higher an individual's perception of the ease of using a system, the higher the level of utilization of information technology.

According to Davis (1989), apart from perceived ease of use, another factor that can influence user intention is perceived trustworthiness. Trust becomes a crucial factor for consumers when deciding to make online purchases. Trust is defined as one party's willingness to accept decisions made by another party, even when the first party is not protected or guaranteed by the second party's actions (Putri & Iriani, 2020). According to research conducted by Zahra, Febrian, and Amar (2019) and Canestren and Saputri (2021), perceived trust has a significant positive impact on the intention to use digital services. However, contrasting results were found in a study conducted by Suprapto and Farida (2022), which showed that the trust variable does not significantly affect the intention to use financial technology.

Perceived risk also plays a significant role in determining an individual's willingness to engage in online transactions. The higher the perceived risk, the greater the fear individuals may have when conducting online transactions. Various types of risks, including psychological, legal, and economic risks, can be of concern. Based on research conducted by Canestren and Saputri (2021) on "The Influence of Trust, Ease of Use, and Risk on Purchase Decisions Using the Shopee Paylater Payment Method" & Prasetyani (2019) on "The Influence of Information Sources, Security, and Perceived Risk on Purchase Decisions in Shopee Marketplace," it has been proven that the risk factor has a significant positive impact on the decision to use the Shopee Paylater payment method. However, a study conducted by Wijaya and Paramita (2017) indicated that the risk factor does not influence online purchase decisions.

Based on the research gaps identified in various previous studies, the author is interested in conducting this research to examine the influence of demographic and geographic conditions on the technology acceptance model regarding the intention to reuse Shopee Paylater among the population in the Solo Raya area, since Surakarta occupies the 3rd position in the highest economic growth in central Java (Suryanto, 2020), supported by Safira, Samudro & Mulyanto (2023), Surakarta City has a very rapid urban growth rate, which can be seen from the economic growth and activity system of the city centers' physical growth. Additionally, this city has been growing significantly with the rise in regional accessibility, marked by the opening of the toll road connecting Jakarta-Semarang-Surakarta-Surabaya (Buchori et al., 2020).

Method

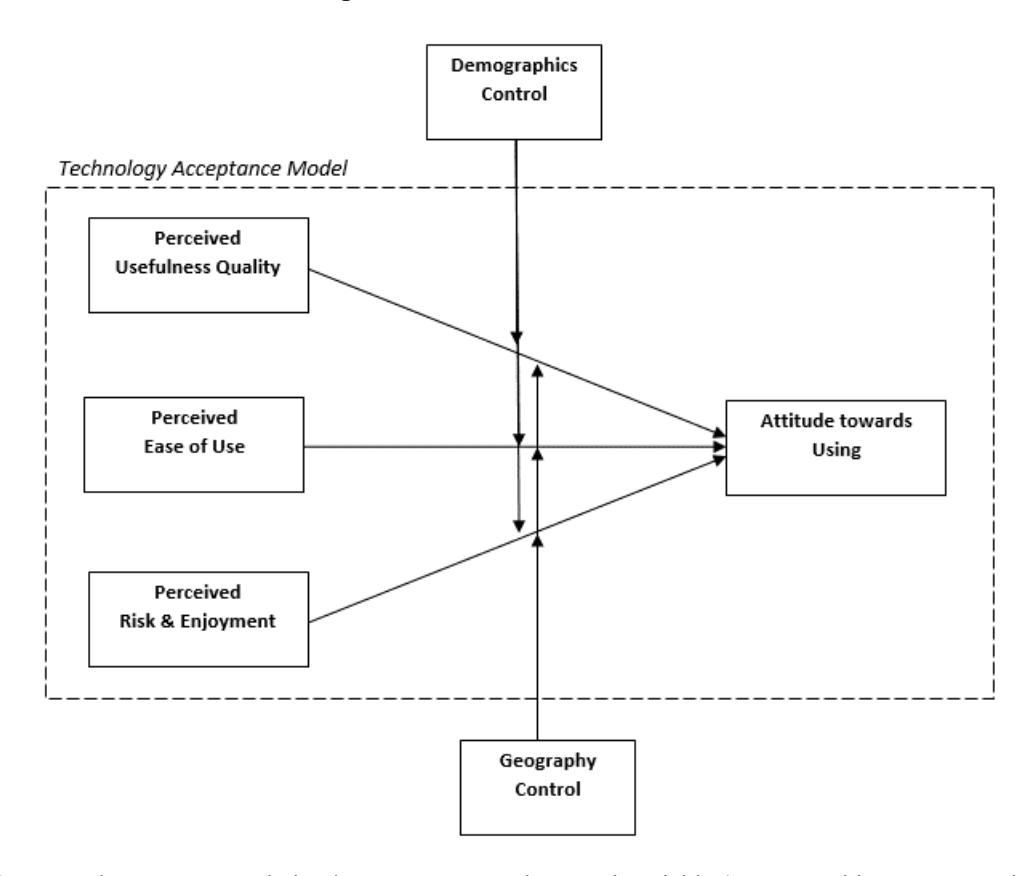

To answer the research question stated above, a quantitative case study research design (Yin, 2018) was conducted using an online survey method among Shopee Paylater users in the Solo Raya region, which consists of the population in Surakarta City and the surrounding districts (Wonogiri, Sukoharjo, Sragen, Boyolali, Klaten, and Karanganyar). The survey results were used to test and validate the research constructs (refer to Figure 1), which consist of the basic TAM model with the addition of two control variables: demographic and geographic variables. Quantitative analysis was employed to examine the relationships between dependent and independent variables. The analysis was conducted using SPSS 26 software, which involved classical assumption tests and statistical tests.

Figure 2 Research Construct: Relation between TAM and Control Variable (Demographics & Geography)

The independent variables in this study are perceived trust, ease of use, and risk, while the dependent variable is the intention to reuse Shopee Paylater. Data collection for this research was conducted using a survey method through Google Forms, which were distributed through various social media platforms such as WhatsApp, Instagram, and Telegram. The links to the Google Forms were shared in Solo community groups and directly sent to respondents through personal chat. Additionally, questionnaires were distributed through "intercept" interviews, where respondents were approached and interviewed in crowded places such as malls and coffee shops in Solo City. The criteria for questionnaire completion were that respondents had made at least one transaction using Shopee Paylater.

According to Hair (2010), the ideal and representative sample size depends on the number of indicators multiplied by 5-10. In this study, there are 20 questionnaire items. The minimum sample size for this research is calculated as 20 x 5 = 100, while the maximum sample size is 20 x 10 = 200. Therefore, a sample of 150 respondents will be selected, as it is considered sufficient to represent the population and meets the minimum sample size requirement. After data collection, validity and reliability tests will be conducted, followed by classical assumption tests to ensure the suitability of the multiple linear regression model.

The validity test in this study was carried out using the product moment correlation technique from Pearson, namely by comparing the value of the rcount with the rtable.

Table I The Results of Validity Test

| Variable | Item Question | R calculated | R table | Explanation |

|---|---|---|---|---|

| Perception of ease of use | X1.1 | 0.630 | 0.306 | Valid |

| X1.2 | 0.472 | 0.306 | Valid | |

| X1.3 | 0.605 | 0.306 | Valid | |

| X1.4 | 0.594 | 0.306 | Valid | |

| X1.5 | 0.631 | 0.306 | Valid | |

| Trust | X2.1 | 0.471 | 0.306 | Valid |

| X2.2 | 0.648 | 0.306 | Valid | |

| X2.3 | 0.721 | 0.306 | Valid | |

| X2.4 | 0.598 | 0.306 | Valid | |

| X2.5 | 0.826 | 0.306 | Valid | |

| Risk | X3.1 | 0.587 | 0.306 | Valid |

| X3.2 | 0.601 | 0.306 | Valid | |

| X3.3 | 0.529 | 0.306 | Valid | |

| X3.4 | 0.651 | 0.306 | Valid | |

| X3.5 | 0.377 | 0.306 | Valid | |

| X3.6 | 0.606 | 0.306 | Valid | |

| Intention to reuse | Y1.1 | 0.748 | 0.306 | Valid |

| Y1.2 | 0.627 | 0.306 | Valid | |

| Y1.3 | 0.681 | 0.306 | Valid | |

| Y1.4 | 0.393 | 0.306 | Valid | |

Source: Processed Primary Data, 2023

The results of the validity test of the independent variable questions (perceived convenience, trust, and risk) and the dependent variable (intention to reuse Shopee Paylater) show that the value of r count > r table, it can be concluded that each research variable instrument is declared valid.

Table II The Results of Linearity Test

| Variable | Deviation from Linearity | Information |

|---|---|---|

| MPU*Ease of Use | 0.124 | Linear |

| MPU*Trust | 0.365 | Linear |

| MPU*Risk | 0.197 | Linear |

Source: Processed Primary Data, 2023

If the deviation from the linearity significance value is greater than 0.05, it can be concluded that between the variables Ease (X1), Trust (X2), Risk (X3), and Interest in Reuse (Y) there is a linear relationship. The reliability test in this study was carried out by looking at the value of Cronbach Alpha through the SPSS program. Variable reliability is said to be good if the Cronbach Alpha value is > 0.70. The results of the reliability test can be seen in the table below:

Table III The Results of Reliability Test

| Variable | Cronbach's Alpha | N of items |

|---|---|---|

| Ease to Used | 0.860 | 5 |

| Trust | 0.852 | 5 |

| Risk | 0.753 | 6 |

| Intention to Used | 0.773 | 4 |

Source: Processed Primary Data, 2023

Table III shows that each variable has a Cronbach's Alpha greater than 0.70, so it can be concluded that the research instrument is reliable and consistent, and the research data is declared reliable.

Table IV The Results of Multicollinearity Test

| Coefficientsa | |||||

|---|---|---|---|---|---|

| Collinearity Statistics | |||||

| Model | Tolerance | VIF | |||

| 1 | (Constant) | ||||

| Gender | .728 | 1.374 | |||

| Age | .839 | 1.192 | |||

| Income | .897 | 1.115 | |||

| Region | .700 | 1.429 | |||

| Perceived of ease of use | .553 | 1.810 | |||

| Trust | .544 | 1.837 | |||

| Risk | .900 | 1.111 | |||

Source: Processed Primary Data, 2023

The multicollinearity test is carried out by looking at the VIF value and tolerance value. If the VIF value is below 10 and the tolerance value is above 0.1, it can be said that there is no multicollinearity between the independent variables. Based on the results of the multicollinearity test, it can be seen that the VIF value of all variables is below 10 and the tolerance value is above 0.1, so that multicollinearity does not occur between variables.

Table V The Results of Glejser Test

| Coefficientsa | |||||||

|---|---|---|---|---|---|---|---|

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | |||

| B | Std. Error | Beta | |||||

| 1 | (Constant) | 104 | .848 | 122 | .903 | ||

| Gender | .014 | .238 | .006 | .058 | .954 | ||

| Age | 066 | .269 | 022 | 247 | .805 | ||

| Income | .359 | .254 | .122 | 1.416 | .159 | ||

| Region | 016 | .237 | 007 | 068 | .946 |

|---|---|---|---|---|---|

| Ease to Used | .071 | .046 | .170 | 1.544 | .125 |

| Trust | .032 | .047 | .074 | .671 | .503 |

| Risk | 031 | .028 | 095 | -1.107 | .270 |

a. Dependent Variable: Abs_RES

Source: Processed Primary Data, 2023

The heteroscedasticity test was carried out to test whether the regression model has variance dissimilarity from the residuals between one observation and another (heteroscedasticity). To see the existence of heteroscedasticity, the Park Glejser Test method was used, which was obtained from the output of the SPSS version 26 program. The results of the heteroscedasticity test that had been carried out showed that there were no heteroscedasticity events. This can be seen from the significant probability of showing a number above the 5% confidence level.

Table VI Regression Analysis Results with Demographic and Geographic Control Variables

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | Collinearity Statistics | |||

|---|---|---|---|---|---|---|---|---|

| B | Std. Error | Beta | Tolerance | VIF | ||||

| (Constant) | .659 | 1.380 | .477 | .634 | ||||

| Perceived ease of use | .309 | .075 | .346 | 4.148 | .000 | .553 | 1.810 | |

| Trust | .171 | .077 | .186 | 2.218 | .028 | .544 | 1.837 | |

| 1 | Risk | .244 | .045 | .353 | 5.408 | .000 | .900 | 1.111 |

| JK | 624 | .386 | 118 | -1.618 | .108 | .728 | 1.374 | |

| Gender | .252 | .437 | .039 | .575 | .566 | .839 | 1.192 | |

| Income | 790 | .413 | 125 | -1.913 | .058 | .897 | 1.115 | |

| Region | .606 | .383 | .117 | 1.582 | .116 | .700 | 1.429 | |

a. Dependent Variable: MPU

Source: Processed primary data, 2023

Based on Table VI, the regression equation can be obtained as follows:

\[\text{[rumus tidak dapat ditampilkan dengan baik — lihat PDF asli]}\]

Based on the regression results, it can be inferred that ease of use, trust, and risk have a positive relationship with the intention to reuse Shopee Paylater. The ease-of-use variable has the largest influence on the intention to reuse Shopee Paylater, as indicated by a coefficient value of 0.309. It is followed by the risk variable with a coefficient value of 0.244 and the trust variable with a coefficient value of 0.171. On the other hand, the demographic and geographic control variables in this research model do not have a significant impact. This means that gender, age, and income differences do not show significant differences. Additionally, the differences in residential areas, both within and outside Solo City, do not have a significant influence on the model.

Table VII Coefficient of Determination Test Results

| Model Summaryb | ||||||

|---|---|---|---|---|---|---|

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | ||

| 1 | .925a | .855 | .753 | 152.280 | ||

b. Dependent Variable: Y_TOTAL

Source: Processed primary data, 2023

Based on table VII, the coefficient of determination (R square) value is 0.753. This means that 75.3% of the Shopee Paylater Reuse Interest variable can be explained by the convenience, trust, and risk variables, while the remainder (100% - 75.3% = 24.7%) is explained by other causes outside the model.

Discussion

The discussion in this research uses one dependent variable, namely Reuse Intention, and three independent variables, namely the Influence of Perceived Ease of Use, the Influence of Perceived Trust, and the Influence of Risk, with demographic control variables such as age, gender, income, and geographical control variable of user residence classified as living outside the city of Solo and living within the city. The findings and discussions for each variable are as follows:

1. The Influence of Perceived Ease of Use on Reuse Intention of Shopee Paylater

Based on the hypothesis testing results, it was found that the perceived ease of use variable has a coefficient value of 0.309 and a significance value of 0.00, which is smaller than 0.05. Therefore, the calculation of the perceived ease of use variable yielded the result that perceived ease of use has a significant positive effect on the reuse intention of Shopee Paylater. This research finding supports the Technology Acceptance Model (TAM) theory proposed by Davis (1989). The findings of this study are consistent with the research findings by Saputri & Pratama (2021), Asja, Susanti & Fauzi (2021), and Sati & Ramaditya (2019). Perceived ease of use influences the reuse intention of Shopee Paylater because the respondents have experienced the ease of using Shopee Paylater and have the belief that Shopee Paylater will always provide convenience for its users. The research findings indicate that perceived ease of use influences the reuse intention of Shopee Paylater among the residents of Kota Solo Raya. This is because the residents of Kota Solo Raya are digitally literate and find it easy to use Shopee Paylater according to their preferences.

2. The Influence of Perceived Trust on Reuse Intention of Shopee Paylater

Based on the hypothesis testing results, it was found that the trust variable has a coefficient value of 0.171 and a significance value of 0.028, which is smaller than 0.05. Therefore, the calculation of the perceived trust variable yielded the result that perceived trust has a significant positive effect on the reuse intention of Shopee Paylater. This research finding is consistent with the Technology Acceptance Model (TAM) theory proposed by Davis (1989). The findings of this study support the research conducted by Canestren & Saputri (2021) which said that trust is built on the expectation that others will act according to the needs and desires of consumers. The analysis results for this variable prove that Shopee Paylater users trust that their expectations are fulfilled, and there is no disappointment in using Shopee Paylater. However, these analysis results do not support the research conducted by Sati & Ramaditya (2019), which states that trust does not have an influence on the intention to use e-money. This research found that trust influences the residents of Kota Solo Raya in their intention to reuse Shopee Paylater. This happens because the expectations of the residents of Kota Solo Raya in using Shopee Paylater are met according to their needs and desires, resulting in no disappointment in using Shopee Paylater.

3. The Influence of Risk on the Reuse Intention of Shopee Paylater

Based on the hypothesis testing results, it was found that the risk variable has a coefficient value of 0.244 and a significance value of 0.00, which is smaller than 0.05. Therefore, the calculation of the perceived risk variable yielded the result that perceived risk has a significant positive effect on the reuse intention of Shopee Paylater. The analysis results for the perceived risk variable support the research conducted Sati & Ramaditya (2019). According to the theory proposed by Pavlou (2003), consumers define risk as their perception of uncertainty and potential negative consequences associated with the use of a product or service. The testing results indicate that the risk variable has a positive and significant influence because users do not experience losses as a result of using Shopee Paylater. In this study, it was found that perceived risk influences the residents of Kota Solo Raya in their reuse intention of Shopee Paylater due to the uncertainty of potential losses associated with using Shopee Paylater. When the perceived risk is high, the motivation of the residents of Kota Solo Raya to reuse Shopee Paylater decreases. People minimize potential losses by evaluating their experience with Shopee Paylater.

4. The Influence of Gender Demographic Factor on the Reuse Intention of Shopee Paylater

Based on the hypothesis, testing results for the gender demographic factor control variable, a coefficient value of 0.624 and a significance value of 0.108 were obtained, which is greater than 0.05. Therefore, in this calculation, it can be concluded that the gender demographic factor control variable does not have a significant and negative effect on the reuse intention of Shopee Paylater. In today's era, both men and women have diverse needs and desires. According to Indarto & Dananti (2021), women tend to be better at managing personal finances and debts with good strategies compared to men. The analysis results for the gender demographic factor control variable also support the research conducted by Herlindawati (2017), which proves that gender does not have a significant and negative effect on consumer behavior. However, these results do not support the research conducted by Astari & Widagda (2014), which found that gender has a significant effect on impulsive purchases, with women being more likely to engage in impulsive buying compared to men. In this study, it was found that gender does not influence the reuse intention of Shopee Paylater among the residents of Kota Solo Raya. This is because both men and women in Kota Solo Raya have high living standards and social needs that need to be fulfilled. This can be seen from the nearly identical response percentages between male and female respondents.

5. The Influence of Age Demographic Factor on the Reuse Intention of Shopee Paylater

The hypothesis testing results for the age demographic factor control variable showed a coefficient value of 0.252 and a significance value of 0.566, which is greater than 0.05. Therefore, it can be concluded that the age demographic factor control variable does not have a significant and positive effect on the reuse intention of Shopee Paylater. These findings do not support the research conducted by Arinda (2015), which stated that age has a significant negative influence on borrowing activities at banks. However, based on the research conducted by Mukmin et al. (2021), age does not have a significant effect due to the development of information and digital services that facilitate users in financial literacy, which forms the basis for the dominance of online loan services among individuals aged 19-34. The results of this study found that age does not influence the reuse intention of Shopee Paylater among the residents of Kota Solo Raya. This is because easy access to information and digital services related to online loans, such as Shopee Paylater, has been facilitated by the advancements in information technology. This is supported by a survey conducted by the Association of Internet Service Providers in Indonesia during the period 2019-2021, which recorded changes in internet usage behavior due to the COVID-19 pandemic. The frequency of internet usage increased by 53.99% among individuals aged 19-34.

- 6. The Influence of Income Demographic Factor on the Reuse Intention of Shopee Paylater

- The hypothesis testing results for the income demographic factor control variable showed a coefficient value of 0.790 and a significance value of 0.58, which is greater than 0.05. Therefore, it can be concluded that the income demographic factor control variable does not have a significant effect on the reuse intention of Shopee Paylater. This may be because the respondents in this study are members of the general public from various occupations with different income levels, leading to variations in how they allocate their income. Whether respondents have high or low income, if it is not aligned with their needs, their intention to use Shopee Paylater may increase. These findings support the research conducted by Purwidianti & Mudjiyanti (2016), which stated that income level has a non-significant negative effect on financial behavior. Additionally, these results align with the research conducted by Rizkiawati & Asandimitra (2018), which found that demographic factors such as gender, age, and income do not significantly affect financial management behavior. However, the results of this analysis do not support the research conducted by Mahendra & Ardiani (2015), which demonstrated that demographic factors such as age, education, and income have a significant positive effect on purchasing intention. In this study, it was found that income does not influence the reuse intention of Shopee Paylater among the residents of Kota Solo Raya. The respondents in this study come from various income levels, and the people of Kota Solo Raya maintain their expected living standards regardless of whether they have a low or high income. This consumer behavior is influenced by technological dependence and the consumption of fuel for transportation (Kurniati et al., 2021). This affects personal financial management, and individuals with both high and low incomes may use Shopee Paylater.

- 7. The Influence of Geographic Factors on the Reuse Intention of Shopee Paylater

The hypothesis testing results for the geographic factor control variable showed a coefficient value of 0.606 and a significance value of 0.116, which is greater than 0.05. Therefore, it can be concluded that the geographic factor control variable has a positive but non-significant effect on the reuse intention of Shopee Paylater. These results contradict the research conducted by Hadiyat (2014), which stated that geographic location is a significant factor influencing people's access to the internet. In this study, the respondents were spread across both the central area of Kota Solo and the surrounding areas (Karanganyar, Sragen, Boyolali, Klaten, Sukoharjo, and Wonogiri), where it can be observed that infrastructure development in Kota Solo Raya is becoming more evenly distributed. Therefore, the geographic location, whether in the city center or on the outskirts, does not significantly impact the use of technology. The influence of globalization is strong in all dimensions of community life, leading to social changes in both rural and urban environments.

Conclusion

Gender, age, and income as demographic indicators and control variables do not affect the reusage intention of Shopee Paylater among the residents of Kota Solo Raya. This is because of the easy access to information and digital services, which transcends gender, age, and income levels. Similarly, the geographic aspect of the place of residence as a control variable does not influence the reusage intention of Shopee Paylater among the residents of Kota Solo Raya. This is likely due to the even distribution of infrastructure development in Kota Solo Raya, which facilitates people's access to technology and digital services. In conclusion, the demographic and geographic conditions of the residents of Solo Raya do not impact their interest in using technology, specifically Shopee Paylater. Further research is needed in other areas to determine whether equitable development in terms of demographic and geographic aspects affects the utilization and adoption of technology.

The research concludes that the perceived ease of use is a significant factor affecting the intention to reuse Shopee Paylater. Therefore, it is crucial for the company to continuously improve the perception of user-friendliness among the community while maintaining the ease of using the Shopee Paylater

feature. Furthermore, the trust variable also plays a significant role in influencing the intention to reuse Shopee Paylater. As a result, it is expected that Shopee maintains the trust of the residents of Solo Raya by promptly addressing user complaints regarding Shopee Paylater. Additionally, the research indicates that the perceived risk variable has an impact on the intention to reuse. Therefore, Shopee is strongly advised to ensure data security and protect the confidentiality of Shopee Paylater user information. For future researchers, it is recommended to broaden the scope of the study by including a larger population beyond the Solo Raya area. Furthermore, researchers are encouraged to explore new variables that can adapt to future circumstances. It would also be beneficial for future researchers to conduct comparative studies on pay-later services available on other platforms, which can strengthen the findings and insights related to existing pay-later services.

References

- Adirinekso, G. P. (2021). Minat dan Penggunaan Fintech PayLater Pekerja Urban Pelangga Traveloka dan GoJek Sebelum dan Selama Pandemi Covid-19 di DKI Jakarta, Journal of Management and Business Review. 18(2), 327-342. https://doi.org/10.34149/jmbr.v18i2.283.

- Andika, I. W. A. & Rastini, N. M. (2013). Pengaruh Variabel Demografi Dan Technology Readiness Terhadap Perilaku Belanja Online Di Kota Denpasar Fakultas Ekonomi Universitas Udayana (UNUD), Bali, Indonesia terhubung menggunakan standar Internet Protocol Suite (TCP / IP) untuk melayani', E-Jurnal Manajemen Universitas Udayana, 2.9, 1160–1174.

- Arinda, N. (2015). Analisis Pengaruh Usia, Jumlah Tanggungan Dalam Keluarga, Pengalaman Usaha, Omzet Usaha dan Jumlah Pinjaman Terhadap Tingkat Pengembalian Kredit Oleh UMKM. Studi Kasus: Bank Perkreditan Rakyat (BPR) Gunung Ringgit Malang, Jurnal Ilmiah Mahasiswa Fakultas Ekonomi dan Bisnis: Universitas Brawijaya, 3(2), 1–12.

- Asja, H. J., Susanti, S. & Fauzi, A. (2021). Pengaruh Manfaat, Kemudahan, dan Pendapatan terhadap Minat Menggunakan PayLater: Studi Kasus Masyarakat di DKI Jakarta (The Influence of Perceived Usefulness, Ease of Use and Income on Interest in Using PayLater: A Case Study of People in DKI Jakarta), Jurnal Akuntansi, Keuangan, dan Manajemen, 2(4), 309– 325.

- Astari, L. & Widagda K., I. (2014). Pengaruh Perbedaan Jenis Kelamin Dan Kontrol Diri Terhadap Keputusan Pembelian Impulsif Produk Parfum, E- Jurnal Manajemen Universitas Udayana, 3(3), 254-840.

- Auralia, Y., Manggabarani, A. S. & Wahyudi, W. (2022). Analisis Minat Penggunaan Ulang pada Dompet Digital Shopeepay di Masa Pandemi Covid-19', Studi Ilmu Manajemen dan Organisasi, 1(2), 137– 152. doi: 10.35912/simo.v1i2.916.

- Buchori, I., Pangi, P., Pramitasari, A., Basuki, Y., & Sejati, A.W. (2020). Urban Expansion and Welfare Change in a Medium-sized Suburban City: Surakarta, Indonesia. Environment and Urbanization Asia, 11(1) 78–101. DOI: 10.1177/0975425320909922

- Canestren, I .A., & Saputri, M. E. (2021). Pengaruh Kepercayaan, Kemudahan, Dan Resiko Terhadap Keputusan Pembelian Menggunakan Metode Pembayaran Shopee PayLater, eProceedings of Management, 8(3), 1-15.

- Chaldun, U. I. (2016). Terhadap Kepedulian Lingkungan studi expost Facto di SMA Negeri 7 Depok tahun 2015 Influence Of Gender Difference And Knowledge About The Basic Concepts Of Ecology On Environmental Concern: ex Post Facto study in SMAN 7 Depok in 2015, 14 117–132.

- Davis, F. D. (1989). Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology, MIS Quarterly: Management Information Systems, 13(3), 319–339. https://doi. org/10.2307/249008

- Dewi, S. K. & Sudaryanto, A. (2020). Validitas dan Reliabilitas Kuesioner Pengetahuan, Sikap dan Perilaku Pencegahan Demam Berdarah, Seminar Nasional Keperawatan Universitas Muhammadiyah Surakarta (SEMNASKEP), 73–79.

- Febriyani, D. A. (2018). Pengaruh Persepsi Kemudahan Penggunaan Dan Persepsi Kemanfaatan Terhadap Minat Beli Online Pada Mahasiswa Ust Yogyakarta Pengguna Zalora. Journal of Chemical Information and Modeling, 53(9),1689–1699. http://jurnalfe.ustjogja.ac.id/index.php/ ekobis/article/view/873

- Fikri, A. (2021). Pengaruh Penggunaan Shopeepay Sebagai Dompet Digital Terhadap Perilaku Konsumtif Mahasiswa FEB USU', Jurnal KomunikA: Komunikasi Massa, Komunikasi Antarpribadi, Komunikasi Antar Budaya dan New Media, 17(2), 1–11. https://doi.org/10.32734/komunika. v17i2.7556

- Financial Stability Board (2017). Financial Stability Implications from Fintech: Supervisory and Regulatory Issues that Merit Authorities' Attention, Financial Stability Board, 1–61.

- Fitriana, B. (2015). Pengaruh Usia, Pendidikan, Pendapatan, Faktor Sosial, Budaya, Pribadi, Dan Motivasi Terhadap Persepsi Konsumsi Pangan Pokok Non Beras Di Wilayah Jakarta Barat, Skripsi Mahasiswa, Fakultas Ekonomi dan Bisnis UIN Syarif Hidayatullah, Jakarta.

- Grace, D., Tanciga, M. S., & Nurdin, N. (2018). Sistem Informasi Letak Geografis Penentuan Jalur Tercepat Rumah Sakit Di Kota Palu Menggunakan Algoritma Greedy Berbasis Web. JESIK: Jurnal Elektronik Sistem Informasi dan Komputer, 4(2), 59-76.

- Gujarati, D. N., & Porter, D. C. (2009). The McGraw-Hill Series Economics (N. Fox (ed.); 5th ed.). Doiglas Reiner.

- Hadiyat, Y. D. (2014). Kesenjangan Digital di Indonesia (Studi Kasus di Kabupaten Wakatobi). Jurnal Pekommas, 17(2), 81–90. https://doi.org/10.30818/jpkm.2014.1170203

- Hamizar, A. (2003). Pergeseran Perilaku Konsumen dalam Minat Beli Ulang Berdasar Produk Website (Analisis Perubahan Model Bisnis terhadap Pilihan Konsumen, TAHKIM: Jurnal Hukum dan Syariah, 16(1), 129–140. http://dx.doi.org/10.33477/thk.v16i1.1458

- Hardhika, R. E. B., & Huda, A. M. (2021). Pengalaman Pengguna Pay Later Mahasiswa di Surabaya, the Commercium, 4(2):19-32, https://ejournal.unesa.ac.id/index.php/Commercium/article/view/41291

- Herlindawati, D. (2017). Pengaruh Kontrol Diri, Jenis Kelamin, Dan Pendapatan Terhadap Pengelolaan Keuangan Pribadi Mahasiswa Pascasarjana Universitas Negeri Surabaya. Jurnal Ekonomi Pendidikan Dan Kewirausahaan, 3(2), 158–169. https://doi.org/10.26740/jepk.v3n2.p158-169

- Husain, T. (2017). Analisis Determinan Faktor-Faktor Yang Mempengaruhi Niat Penggunaan Software Audit. Jurnal Ilmiah Matrik, 19(2), 131–150. https://doi.org/10.33557/jurnalmatrik.v19i2.381

- Ilman, A. H., Noviskandariani, G., & Nurjihadi, M. (2019). The Role of FinTech on The Economy of Developing Countries. Jurnal Ekonomi Dan Bisnis Indonesia, 4(1). https://doi.org/10.37673/jebi. v4i1.260

- Indarto, D. N. S., & Dananti, K. (2021). Pengaruh Perilaku Konsumtif, Jenis Kelamin, dan Pendapatan terhadap Pengelolaan Keuangan Pribadi Karyawan Divisi Garment PT Dan Liris Sukoharjo. Jurnal Manajemen Bisnis Dan Kewirausahaan, 5(5), 558–562. https://doi.org/10.24912/jmbk.v5i5.10327

- Jagadhita, P. A. A., & Tjhin, V. U. (2023). Analysis of Factors Influencing Intention to Use Pay Later Using Technology Acceptance Model (TAM). Jurnal Cahaya Mandalika, 4(1), 467-479. https:// doi.org/10.36312/jcm.v4i1.1356.

- Joseph, William, Barry, dan Rolph. (2010). Multivariate Data Analysis 7th Edition. United States: Pearson Education.

- Kurniati, S. D., Rahman, A., & Trinugraha, Y. H. (2021). Komunitas Joli Jolan Mencegah Perilaku Konsumtif Masyarakat Di Solo, 10(2), 226–236. https://doi.org/10.23887/jish-undiksha. v10i2.32285

- Mahendra, M. M. & Ardiani, I. G. A. K. S. (2015). Pengaruh Umur, Pendidikan dan Pendapatan Terhadap Niat Beli Konsumen pada Produk Kosmetik The Body Shop di Kota Denpasar, Fakultas Ekonomi Universitas Udayana, Bali, Indonesia, 442–456.

- Mention, A. L. (2019). The Future of Fintech, Research-Technology Management, 62:4, 59-63, https:// doi.org/10.1080/08956308.2019.1613123.

- Nizar, M.A. (2020). Financial Technology (Fintech): It's Concept and Implementation in Indonesia, Munich Personal RePEc Archive, 5(98486), 4–10.

- Mukmin, M. N., Masnuneh, M., Warizal, & Ch, I. (2021). Pinjaman Online: Pengetahuan, Tabungan, Asuransi, dan Investasi. Jurnal Sosial Humaniora, 12(2), 171–177. https://doi.org/10.30997/jsh. v12i2.4683

- Pavlou, P. A. (2003). Consumer Acceptance of Electronic Commerce : Integrating Trust and Risk with the Technology Acceptance Model, International Journal of Electronic Commerce, 7(3), 69–103. https://doi.org/10.1080/10864415.2003.11044275

- Prasetyani, I. & Wahyuningsih, T. H. (2019). Pengaruh Sumber Informasi, Keamanan, Dan Persepsi Resiko Terhadap Keputusan Pembelian Pada Marketplace Shopee, Efektif Jurnal Bisnis dan Ekonomi, 10(1), 91–104.

- Priskilia, P., & Sitinjak, T. (2020). Pengaruh Iklan, Promosi Penjualan, Dan Persepsi Kemudahan Penggunaan Terhadap Minat Memakai Ulang Layanan Go-Pay Di Wilayah Jakarta. Jurnal Manajemen, 9(1). https://doi.org/10.46806/jm.v9i1.607

- Purwanto, N. (2019). Variabel Dalam Penelitian Pendidikan, Jurnal Teknodik, 6115, 196–215.

- Purwidianti, W. & Mudjiyanti, R. (2016). Analisis Pengaruh Pengalaman Keuangan Dan Tingkat Pendapatan Terhadap Perilaku Keuangan Keluarga Di Kecamatan Purwokerto Timur, Benefit: Jurnal Manajemen dan Bisnis, 1(2), 141. https://doi.org/10.23917/benefit.v1i2.3257

- Putri, F. A., & Iriani, S. S. (2020). Pengaruh Kepercayaan dan Kemudahan terhadap Keputusan Pembelian Menggunakan Pinjaman Online Shopee PayLater. Jurnal Ilmu Manajemen, 8(3), 818–828. https:// doi.org/10.26740/jim.v8n3.p818-828

- Putri, S. E., Safitri, H. & Hariyanto, D. (2023). The effect of financial literacy and technology acceptance model on interest in using shopee paylater in students, INOVASI: Jurnal Ekonomi, Keuangan dan Manajemen, 19(1), 64–72.

- Rahmad, A. D., Astuti, E. S. & Riyadi (2017). Pengaruh Kemudahan Terhadap Kepercayaan dan Penggunaan SMS Banking (Studi pada Mahasiswa Jurusan Administrasi Bisnis Universitas Brawijaya), Jurnal Administrasi Bisnis, 43(1), 36–43.

- Rafi, I. P. (2021). Analisis Faktor Penggunaan Dompet Digital Di Kalangan Mahasiswa Perguruan Tinggi Surabaya, JATISI: Jurnal Teknik Informatika dan Sistem Informasi, 8(1), 312–322. https://doi. org/10.35957/jatisi.v8i1.584

- Rakasiwi, L. S. & A. Kautsar (2021). Pengaruh Faktor Demografi dan Sosial Ekonomi terhadap Status Kesehatan Individu di Indonesia, Kajian Ekonomi dan Keuangan, 5(2), 146–157. https://doi. org/10.31685/kek.v5i2.1008

- Ratu, A., Subali, E., Marsudi., Prasetyo,B., Fahmi,A. Zahrok,S., Hendrajati,S., Prasetyawati,N., Satya,D., Rintaningrum, R. (2019). Analisa Pengaruh Faktor Sosio-Demografi Terhadap Penggunaan Media Sosial Sebagai Sarana Berbisnis. Journals of Economics Development Issues, 2(2), 1-8.

- Renny, Guritno, S. & Siringoringo, H. (2013). Perceived Usefulness, Ease of Use, and Attitude Towards Online Shopping Usefulness Towards Online Airlines Ticket Purchase, Procedia - Social and Behavioral Sciences, 81, 212–216. https://doi.org/10.1016/j.sbspro.2013.06.415

- Rizkiawati, N. L. & Asandimitra, N. (2018). The Influence of Demography, Financial Knowledge, Financial Attitude, Locus of Control and Financial Self-Efficacy on the Financial Management Behavior of the Surabaya Community, Jurnal Ilmu Manajemen, 6(3), 2.

- Safira, L. Samudro, B.R. & Mulyanto (2023). Determination of the Center for Economic Growth in Surakarta City, Indonesia: Geospatial Approach. International Journal of Sustainable Development and Planning, 18(9), 2801-2810. https://doi.org/10.18280/ijsdp.180918

- Saputri, D. A & Pratama, R. A (2021) Classifying Users of Indonesia's Top-five e-Wallet Services with MCA. Jurnal Sosioteknologi. 20(2), 138-148. https://journals.itb.ac.id/index.php/sostek/article/ view/15848

- Saputri, M. (2022). The Effect of Performance expectation, Effort expectancy, social influence, perceived risk, and perceived cost on the intention of using mobile payment in Indonesia. Jurnal Sosioteknologi. 21(1), 10-21. https://doi.org/10.5614/sostek.itbj.2022.21.1.2

- Sari, R. (2021). Pengaruh Penggunaan Paylater Terhadap Perilaku Impulse Buying Pengguna E-Commerce di Indonesia. Jurnal Riset Bisnis Dan Investasi, 7(1), 44-57. https://doi.org/10.35313/jrbi.v7i1.2058

- Sati, R. A. S. & Ramaditya, M. (2019). Pengaruh Persepsi Manfaat, Persepsi Kemudahan Penggunaan, Kepercayaan Dan Persepsi Risiko Terhadap Minat Menggunakan E-Money (Studi Kasus Pada Konsumen Yang Menggunakan Metland Card), Management, 1–20.

- Setiawan, W., Sunaryo, D. & A.R, Khorida. (2022). Service Features and Security Analysis of the Use of Digital Wallet (Shopee Pay), Digital Business Journal, 1(1), 52-61. http://dx.doi.org/10.31000/ digibis.v1i1.6602

- Setyawati, N.A. (2022). Pengaruh Kualitas Layanan Dan Kepercayaan Terhadap Minat Pengguna: (Studi Kasus Pada Pengguna Fitur Shopee Paylater). GEMAH RIPAH: Jurnal Bisnis, 2(01), 60–72.

- Setyawati, N.A. (2022). Pengaruh Kualitas Layanan Dan Kepercayaan Terhadap Minat Pengguna (Studi Kasus Pada Pengguna Fitur Shopee Paylater), Undergraduate thesis, Universitas 17 Agustus 1945 Surabaya.

- Siregar, K.R., Rachmawati, I., Millanyani, H. & Esperanza, M. (2022). Ipma Analysis of The Students' Acceptance on The Use of Celoe Learning Management System (LMS), at Telkom University. Jurnal Sosioteknologi, (21)1, 60-69. https://doi.org/10.5614/sostek.itbj.2022.21.1.7

- Suprapto, Y., & Farida, F. (2022). Analisis Pengaruh Brand Image, Trust, Security, Perceived Usefulness, Perceived Ease of Use Terhadap Adoption Intention Fintech Di Kota Batam. Jesya (Jurnal Ekonomi Dan Ekonomi Syariah), 5(1), 319-332. https://doi.org/https://doi.org/10.36778/jesya.v5i1.569

- Suryanto. (2020). The Synergy of Economic Growth, Income Inequality and Poverty in The City of Surakarta. Jurnal Ilmu Ekonomi dan Pembangunan 20(2), 1412-2200. https://jurnal.uns.ac.id/jiep/ article/view/46105

- Sustiyo, J. (2020). Apakah Literasi Keuangan Mempengaruhi Perilaku Konsumsi Generasi Z? Jurnal Manajemen Mandiri Saburai (JMMS) 4(1), 1–10. https://doi.org/10.24967/jmms.v4i1.592

- Venkatesh, V., & Davis, F. D. (2000). A Theoritical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Management Science, 46(2), 186-204. https://doi.org/10.1287/ mnsc.46.2.186.11926

- Yin, R. K. (2018). Case Study Research and Applications: Design and Methods (6th ed.). Thousand Oaks, CA: Sage.

- Zahra, H. A., Febrian, E., & Amar, S. D. (2019). Faktor-Faktor yang Mempengaruhi Sikap dan Intensi Pengurus Koperasi Untuk Menggunakan Platform Layanan Keuangan Digital di Kota Bandung. Jurnal Manajemen (Edisi Elektronik), 10(2), 155–165. https://doi.org/10.32832/jm-uika.v10i2.2572