INFO ARTIKEL

Kata kunci:

Paylater, pola perilaku pengguna, desain perilaku, strategi desain, marketplace

ABSTRAK

Trend cashless dalam transaksi digital telah menggantikan metode pembayaran konvensional dalam kehidupan sehari-hari. Percepatan transformasi digital telah membawa implikasi dampak berkelanjutan di masyarakat. Mulai dari perilaku impulsive buying, maraknya penipuan hingga fenomena pinjaman online. Dalam setiap kemudahan teknologi, terdapat proses dan keputusan desain di dalamnya. Dalam hal ini kemudahan layanan keuangan digital di e-commerce berpengaruh terhadap perubahan pola perilaku pengguna dan gaya hidup baru dalam berbelanja. Penelitian ini memetakan cakupan intervensi desain pada perubahan perilaku dengan kombinasi data literature, ethnography online, survei, dan wawancara sebagai landasan analisis berbagai aspek behavioral design dalam memengaruhi keputusan pengguna. Hasil penelitian ini menyajikan strategi desain yang digunakan pada tahap perubahan perilaku dalam menavigasi layanan Paylater. Penerapan sudut pandang desain perilaku membantu mengidentifikasi efektivitas trigger dari setiap tahapan, sehingga dapat memperkuat desain dan memitigasi atau meminimalisasi risiko interaksi pengguna yang mungkin diabaikan.

Introduction

Design, as a social construction, plays a role in lifestyle transformation. The ability of design to convey meaning through the signs and signifiers of each object created has an impact on how people internalize values as part of their identities, whether personal or collective, and how they reflect lifestyle choices. Design objects facilitate the identification and mapping of an individual's position, potential, and role within the social structure of society.

The combination of design and technology has triggered changes in thought processes, activities, interactions, and behavioral patterns that encourage new lifestyles. These conditions have surrounded people's lives, coexisting side by side with design objects (Kurniawan, 2009). People's interaction patterns with design are becoming increasingly intense in everyday life. The design fosters innovation in user relationships with objects, both in product creation and practice, thereby altering the level of human interaction and its intensity in technology use (Surahman, 2018). Even in certain situations, the design can alter and manipulate environmental conditions to facilitate human interaction (Kurniawan, 2009).

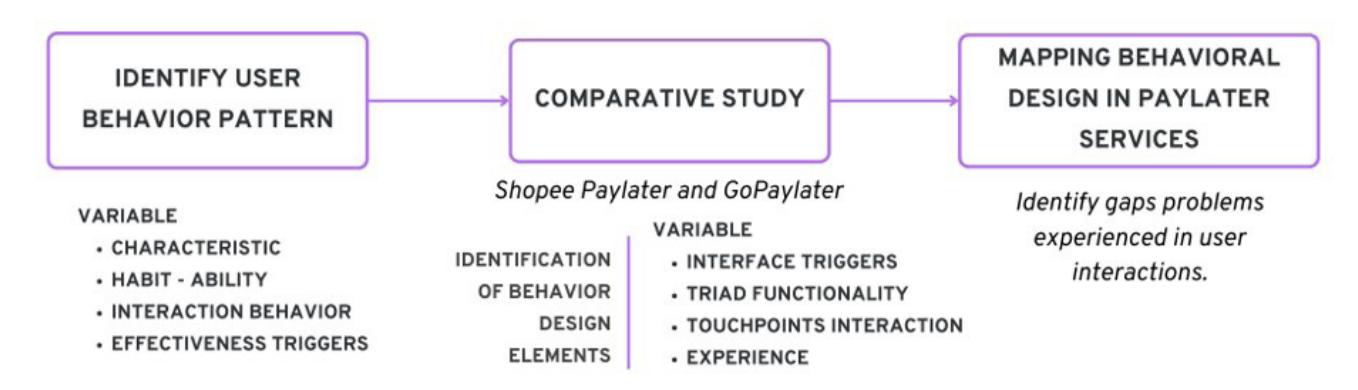

Paylater, a payment alternative in e-commerce that simplifies transactions for users, is gradually beginning to replace credit cards (Parameswari & Ginny, 2022). The adoption of e-wallets has surpassed cashless trends among students, resulting in a change in their daily cash handling behavior (Chelvarayan, et al., 2022). Paylater has significantly increased from two years ago, still surpassing top-up transactions via Alfamart or Indomaret.

The emergence of the phenomenon of shopping behavior using Paylater (Kurniasari & Fisabilillah, 2021), particularly for users who love to shop, makes their lifestyle more consumptive, which is further reinforced by social influence from friends and advertising. Sari (2020) found that the ease of use of Paylater significantly influences users' impulsive buying behavior when they shop on e-commerce. It is known from BNPL data that young people's Paylater installments reach an average of 95 percent of their monthly income. This stands in stark contrast to the typical approved banking installments, which typically represent only 30 percent of income (Respati & Djumena, 2024). This indicates that the convenience offered in Paylater account activation has a significant influence on the characteristics of BNPL users in e-commerce compared to credit at banks. Fashion, data packages, the internet, and electricity dominate Paylater usage, with monthly expenses, electronic needs, accessories, the latest gadgets, and holidays accounting for the remainder.

In response to the phenomenon of the transformation of digital financial services, which encourages the use of Paylater on e-commerce platforms, various implications arise because of changes in the behavior of lifestyle transformation. This necessitates mapping the characteristics and behavior patterns of users when navigating services, as well as considering the implications of lifestyle transformations on society. The analysis of user transaction flow mapping is used to identify design intervention gaps. This analysis serves as a basis for adjusting several required parameters in the development of digital financial applications, particularly Paylater services in e-commerce. This paper aims to contribute to the existing research on the mapping of design relationships in the behavior development process of digital financial services, which in turn leads to new lifestyle changes. This enables the use of adaptive strategies to develop application designs that enhance user transaction flows, responding to the phenomenon of lifestyle transformation.

Relation of Behavioral Design in Lifestyle Transformation

Maja van der Velden et al. (2016) examine design influences on human behavior to achieve sustainability goals and consider social norms and their implications in increasing community participation and support. Behavioral design is an important key practice for overcoming behavioral and social challenges. (Cash et. al., 2022).

Social issues that involve behavior in initiating desired changes mean that we can use the power of design as a means to change behavior (Tromp et al., 2011). Tromp et al. (2011) argue that user experience

has influence and plays an important role in the effectiveness of the behavioral design interventions. In their article, Triharini et al. (2024) highlight the design approach in policy interventions for business actors and its application in program sustainability. By using the power of design to influence people's behavior, designers can contribute to alleviating some of the major social problems we face, including lifestyle changes (Ludden, 2014).

A behavioral design perspective can help in understanding changes in user behavior patterns that encourage new lifestyle transformations from every design decision that carries the possibility of a sustainable impact (Papanek & Fuller, 1972). Modern humans are rapidly changing digital transformation and application development to meet public needs and fend off the threat of digital disruption (Li, 2021; Petersen et al., 2016).

Design failure occurs when there is a mismatch between the user and the object, often resulting in unexpected behavior, misinterpretation, and design adaptation. Therefore, it is crucial to consider the elements that shape lifestyle-related behavioral changes during the design development process. By using the power of design to influence user behavior, design capacity can minimize some of the social problems faced.

Based on the principles of persuasive technology (Fogg, 2003) as a tool, a design can increase capability, as media can provide experience, and as a social actor, it can build relationships. Meanwhile, according to Tromp (2011), user or product interaction design is a way to achieve the desired behavior.

In understanding the problems and needs of target behavior, according to the COM-B Model for Behavior Change, there are three main elements that influence behavior change, namely motivation, capability, and opportunity (Michie et al., 2011; Vliek, 2023). Motivation is used to increase the desire to change conditions. The elements that form motivation include beliefs, attitudes, intentions, and social norms. A design strategy for raising awareness is necessary to build user motivation. It raises users' awareness of objects, shapes their perceptions, and boosts their intentions to act. Meanwhile, ability encompasses habits and task knowledge, typically associated with familiarity. The abilities possessed by users encourage the capability to make changes. An individual's possession of capital creates opportunities and enhances their ability to achieve goals. The existence of options opens a person's allowable actions (opportunity) to achieve certain actions or even act differently from their habits.

In every evolution, design may offer a unique perspective that creates new opportunities, options, or possibilities for addressing an issue in each development. Design builds a value, alters the order, and creates a new reality or function that differs from its previous existence in the environment. In certain contexts, design can either counteract existing problem conditions or serve as a predictor of future problems or perceived risks. This approach can be used to predict the user's spontaneous moments at critical moments in interacting with an object, for example, predicting stressful moments and the user's possible actions at that moment (Rahman, 2016; Jaime, 2014).

Method

Mulyani (2022) defines behavioral research as a combination of methods that measure human behavior, collect new data, and analyze the implications of situations changed through active treatment of human behavior. Behavioral mapping is a technique that describes behavior or activities in an area into a diagram or sketch (Sommer, 1980, cited in Haryadi, 1995).

• This study employed an explanatory design research approach, which integrated data from case studies, questionnaires, interviews, and online ethnography. Quantitative data was used to measure performance (time, frequency, and percentage of task success) as well as the level of effectiveness of features or sections in influencing user decisions. This research identified several relevant Paylater and e-wallet applications integrated with e-commerce, such as Shopee Paylater and GoPaylater at Tokopedia, as a representation of widely used Paylater services. We collected data using an open questionnaire, involving 75 respondents from various regions and backgrounds. We divided the participant criteria into two groups, categorizing them based on their experience and intentions to use Paylater services. The study recorded the following quantitative data:

- • The characteristics of the user include their demographics, income, expenses, and frequency of use.

- • Motivation, ability, and opportunity are factors that shape behavior change.

- • The degree to which a feature or section influences user decisions

- • The user's interaction, habit, and lifestyle have changed.

We utilized qualitative data to delve deeper into reflective, emotional, and behavioral aspects. Qualitative data collection was carried out through interviews and think-aloud protocols combined with online ethnography on several social media platforms to obtain a broader perspective regarding understanding phenomena, experiences, and problems felt by users. This was done to capture users' mental processes, emotions, expectations, and feedback, as well as their actions and behavior when interacting with the product.

Figure 1 Research Scheme and Data Analysis Stage Source: Nada, 2024

The research is divided into three stages. The initial stage is to identify user characteristics and behavior in interacting with the service. This is followed by the service flow mapping stage, which analyzes several parameters to find elements or parts in the application that influence interest and decisions to use the service. The final stage is data interpretation and analysis of gaps in user interaction flow and the application of behavioral design in Paylater services in the marketplace.

Results and Discussion

Human behavior encompasses the actions and interactions of individuals with the environment and involves knowledge, attitudes, and responses to stimuli (Adventus et al., 2019). These activities often develop into behavior patterns, forming habits and shaping their lifestyle. It is crucial to analyze the shifting patterns of user behavior both before and after the rise of Paylater at marketplace.

Functional Triad in Paylater Services

The Fogg Behavior Model (2009) has been instrumental in addressing practical issues in behavior change design, particularly in technology. It aids in understanding the behavior formation and serves as a framework for persuasive analysis and design. The model's functional triad outlines three roles of technology: as a tool, media, and social actor, capturing how users interact with technology products. As a tool, technology influences behavior by simplifying tasks, boosting self-efficacy, providing tailored information, and guiding users through processes. Specifically, in Paylater services, technology functions through physiological cues, such as visually appealing designs, and psychological cues, aligned with user preferences.

Application of BJ Fogg's Persuasive Technology Principles

It serves as a tool for shaping human behavior. As a physiological cue, an object that is visually more attractive to the user will also appear more persuasive. Fogg's principles of persuasive technology have found widespread application across various services. These principles include reduction, tunneling, tailoring, suggestion, conditioning, self-monitoring, and surveillance. Based on the analysis data, the following list of persuasive design concepts in Paylater services and their implications for changing user behavior patterns is provided.

Transition of Credit Users Related to the Reduction Principle

Previously, obtaining a credit card required meeting specific criteria, including age and income thresholds. The advent of Paylater has simplified access to credit, leading to a shift in user segmentation. Data shows that 67.1% of Paylater users are Gen Z students, with 72.6% having no personal income and relying on their parents. These students typically have an income range of IDR 1,500,000 to IDR 2,500,000 and use nearly 90% of their income on expenses. In critical situations, they turn to Paylater for temporary needs. In contrast, workers use about 35% of their income but still utilize Paylater to capitalize on discounts.

Applying the reduction principle to simplify online loan application and activation processes has transformed previously complex interactions into new behaviors. The ease of activating Paylater accounts has expanded access beyond adults with stable incomes to include younger users and students, fostering the habitual use of digital credit. Data shows that students primarily purchase skincare and fashion items, while workers focus on daily necessities, electronics, and bills. Notably, some users prefer Paylater for small items, finding them cheaper, though these transactions can accumulate into significant debt—a scenario less common than Paylater. This simplification has broadened the demographic of credit users, altered the social structure of loan usage, and led to more consumptive behavior compared to traditional bank loans, often exceeding users' financial capacities.

Reduction and Conditioning in Adaptation of Cashless Society

Previously, humans carried out transactions using money as a means of exchanging value. Along with the development of digital transformation, various digital financial service applications continue to emerge as a result of digital industry competition and opportunities. E-wallets, as payment applications, enable users to make purchases more conveniently. Users without income, such as college or university students, can make transactions more frequently due to the offered convenience. This has become a new trend among students who now tend to be cashless, and the use of e-wallets has replaced conventional payment methods (Chelvarayan et al., 2022). So, he rarely carries cash in his daily life. The increasing cashless trend has reduced the number of ATM machines (Simamora, 2024).

In this context, the principles of reduction and conditioning are used to familiarize users with new interaction conditions in transactions, simplify the transaction process through QRIS, and gradually condition society to become a cashless society. In the process of influencing human behavior, design development needs to consider affordance space. Kennewell (2001) asserts that design principles of affordances, constraints, and capabilities can intervene in user activities or actions. Affordances provide information on an object that determines the actions a user may take. Through signifiers formed with specific intentions, designs can direct users through a series of experiences.

The QR code scan feature in Paylater services simplifies transactions by allowing users to pay without needing a balance or visiting an ATM, reducing transaction times and queues. This aligns with the design principle of reducing complex interactions, fostering new behaviors in social interactions between traders and buyers, and encouraging merchants to adapt by providing QRIS scan codes. Allowable action from the affordance of this service gives users the ability to pay for QRIS with Paylater. Naturally, this has led to a shift in user behavior towards cashless transactions due to the convenience of Paylater. From an economic perspective, this is very profitable. However, it turns out there are problems with this digital transaction process. Online ethnography observations revealed user problems with QRIS transactions via e-wallet in daily life.

The convenience offered alters users' behavior during transactions, reducing their awareness of non-physical transactions and the amount of money they spend. This is less likely to occur in cash transactions when there is a relatively large difference in the nominal amount spent. Transaction errors with cash typically result from a lack of care during the transaction, as students rarely carry large amounts of cash. Each user experienced this issue at least once while engaging in digital transactions. 62.6% of respondents reported using e-wallets more frequently than their primary e-commerce services or e-commerce itself. In this situation, there is a tendency for user dependency on e-money to be greater than e-commerce. Data on user dependence on digital transactions, reaching 74.3% of total respondents, reinforces this. An open survey on the X media platform revealed that 58.97% of participants felt more comfortable using cashless money. Users only become aware of the expenditure when they check their balance, as they don't physically feel it. Furthermore, the transaction process can be easily completed by simply scanning the QR code on QRIS, eliminating the need to visit an ATM, even if you don't have a wallet. Meanwhile, 41% of respondents still perceive cash as a more convenient method of payment. Because of the environmental conditions, more people accept cash payments, making cashless transactions considered more economical.

Constraints are instructions that limit the number of possible actions a user can take when interacting with an object, thereby simplifying the product for them. This helps them take appropriate action based on existing constraints. Certain constraints may determine the value of an object. For example, QRIS is considered more powerful for transactions than cash in the context of a cafe that only accepts GoPay. No matter how much cash the user has, its value will not be higher than the e-money balance in the context of this situation. Likewise, in different situations and conditions, millions of rupiah held in an M-banking account are not worth anything in the eyes of traders who only accept cash.

In the realm of online shopping, e-wallets hold a more prominent position than cash, with the exception of stores that accept the COD payment method. Meanwhile, infrastructure conditions in Indonesia are not all evenly distributed. Not every area has easy access to ATM services. Therefore, for online shopping, people in rural areas often rely on minimarkets to top up their e-wallet balance. With the emergence of Paylater as a payment alternative, it appears to be a solution for those who struggle with accessibility to banking services, simplifying the process by eliminating the need to top up your balance at the minimarket for each purchase. You only need to make a deposit once a month to pay Paylater bills. This intensity is what brings users to long-term use of Paylater, which initially begins with the user's constraints and abilities.

Mapping Application of BJ Fogg's Persuasive Technology Principles

Based on the mapping of the principles of technological persuasion in Paylater services in e-commerce, the principles of reduction and conditioning have a lot to do with affordances and constraints related to possible actions taken by users. These two principles serve as the foundation for services that aim to influence and form new behaviors for users during transactions. These principles simplify intricate procedures and help users adjust to these interactions.

Table I Persuasive Technology Principles in Paylater Service

Principle Application and Implications for Behavior

Reduction simplification of an initially complex interaction process

Conditioning directs users to familiarize themselves based on situations/ conditions to form perceptions, affection and behavior

With the ease of account activation provided in terms of policy, process and accessibility.

Figure 2 Reduction Credit Application Process Source left image: CNBC, 2024. Source right image: Nada, 2024.

By reducing complex interactions and getting users used to certain conditions, it can lead to the formation of new interactions in transactions. This is in accordance with the reduction and conditioning principles of design as a persuasive tool. In this context, what is formed is not only new behavior such as digital credit transaction habits, but also changes in user characteristics, many of whom are now students.

Reduction simplification of an initially complex interaction process

Conditioning directs users to familiarize themselves based on situations/ conditions to form perceptions, affection and behavior

By reducing complex interactions and getting users used to certain conditions, it can lead to the formation of new interactions in transactions. Slowly conditioning society into a cashless society.

Figure 3 Affordance in QRIS Paylater Source: Nada, 2024.

In this context, what is emerging is not only new digital transaction behavior, the formation of the habit of buying on credit, but users are also becoming less aware of the amount spent during transactions.

Tunneling

directs users when faced with choices, each charging option is accompanied by a guide

Instructions or guides that direct users can use in the form of highlights or education when faced with charging options. As a result, it becomes easier for users to understand each choice or action to be taken. This has proven to be effective in influencing users, because the use of Paylater for the credit and billing category is in third position.

Figure 4 Tunneling in Transaction Process Source: Nada, 2024.

Suggestion

directs users to pay attention to suggestions according to the conditions they are experiencing.

Example of a suggestion to continue an unfinished order. Recommendations that direct users to suggest certain options according to the conditions they are experiencing. With highlights compared to other options. This can redirect users, especially those who don't have a goal in mind at the start or are still unsure about their choice.

Figure 5 Suggestion Unfinish Transaction and Option Credits Source: Nada, 2024.

Tailoring

directs users to customization to suit their needs, interests, and context of use.

This principle directs users to customize to suit their needs, interests, and context of use. Through the options provided, users can customize their loan needs according to the user's conditions and abilities. This principle provides capital for users to act with easier decision making.

Figure 6 Tailoring Simulation and Option Credits Source: Nada, 2024.

Based on the data obtained, what is formed from this principle not only gives rise to new behavior related to borrowing habits (digital credit transactions), transition in user credits, and user characteristics among students but also weakens the condition of user awareness regarding the amount spent during transactions.

Meanwhile, in influencing and shaping consumption patterns, impulsive buying, and dependency, the principles of tunneling, suggestion, and tailoring can be used, which are often found in user transaction flows when shopping or exploring services. This principle is related to triggers that trigger and encourage user behavior, which will be explained further in the next discussion regarding flow comparisons in several service categories.

Psychological Cue

Psychologically, an object or service that provides similarity or suitability to the user's psychological characteristics will appear more persuasive. Empathetic object displays that align with the user's category often garner preference and usage. Psychological object elements serve as a tool, identifying and enhancing the user's abilities in service interactions.

The visual hierarchy in both services is related to the patterns of user behavior when interacting with the service. From a psychological perspective, this strategy is called buyer's remorse, or the paradox of choice. This theory was developed by Schwartz's (2004), which explains the behavior of consumers who often experience confusion with various product choices with many options placed in one storefront. Iyengar and Lepper (1991) identified the possibility of someone being demotivated by choice and considered someone with many desires to be a beneficial thing. Schwartz distinguishes two types of consumer behavior on online platforms.

Initially, the satisfied consumer type (Simons, 1950) typically selects the product that is directly in front of them, without considering any benchmarks or comparisons with similar products. The second type, Maximizer, as opposed to Satisfier, prioritizes the pleasure or experience of shopping by paying attention to reviews and comparing them with other platforms. Usually, this type tends to take longer to make decisions because of doubts regarding many considerations in the information they have. They consider factors such as price, rating, quality, appearance, material, and more.

Shopee boasts a wide and varied market segmentation. In response to these conditions, Shopee is making every effort to develop a diverse range of features that will appeal to a wide range of market segments. Shopee aims to ensure that consumers of the maximizer type experience pleasure and satisfaction. Shopee displays a multitude of options simultaneously on its main page. This corresponds to the psychological nature of women when shopping. In terms of making purchasing decisions, men and women differ in the following ways: women tend to pay more attention to new things and trends, consider the pleasure aspect (hedonistic consumers), are more impulsive, and are loyal to certain brands (Nuraini, Maria, & Gitosudarmo, 2008). Researchers found that these four factors were present in women. This suggests that more factors are considered when making decisions for women. Tokopedia appears to be pursuing an alternative approach. With a simpler appearance and layout, it can attract male users. This also aligns with men's shopping habits, as they typically concentrate on their desired purchases rather than weighing numerous options. This aligns with the psychology of user decision-making, which identifies personality traits such as assertiveness, reasoning, rationality, and a focus on individual goals as characteristics of masculinity (Palan et al., 2011). From this, it can be interpreted that most men belong to the satisfied type in decision-making, based on their masculine personalities, which tend to focus on goals, so they are more satisfied when shopping at Tokopedia.

Shopee typically utilizes interactive features like ShopeeLive, Flashsale, and ShopeeVideo to grab users' attention at the beginning of the page, followed by product recommendations. Tokopedia, on the other hand, has adopted a different strategy, focusing on product recommendations rather than emphasizing flash sales. These differences are significant in their contribution to influencing consumer behavior patterns and preferences for each service. This can be identified as a psychological object element that enhances users' transactional abilities by encouraging longer interactions with the service.

Figure 7 Service Interaction is Associated with the Original Situation of the Shopping Center Source: Modified from Youtube and Nada personal documentation, 2024.

The similarity or suitability of this marketplace service can be associated with previously existing shopping centers or supermarkets. Shopee's strategy in attracting user attention at the start can be associated with the type of hard selling that usually occurs in shopping center aisles, as seen in the picture above. This is related to the psychological aspect of users who associate the service with the original situation at the shopping center so that the service adaptation process can be easier. Apart from that, the placement of ShopeeLive and ShopeeVideo at the beginning of the page is also similar to the placement of outdoor merchants on the first floor of a shopping center. Users entering and leaving the service are easier to reach. This can also be interpreted as social cues from the service, especially in efforts to model target behavior or attitudes, as well as providing social support based on interactive situations.

Women's behavior patterns and habits in shopping can also be observed. Based on the respondents obtained, most female users' interactions with e-commerce platforms tend to scroll or look at interesting and funny-looking items until they feel satisfied and find what they feel is the most affordable price. This behavioral pattern has existed and been a habit since before e-commerce existed. The past shows that women in the mall browse the display cases, which display necessities by category. This behavioral pattern is carried over when using e-commerce applications. Because it has become a habit, whatever the platform, the behavior remains like that. This habit can become capital as an ability to reach various types of transactions, encouraging impulsive buying and the use of Paylater in purchases.

This buyer's paradox condition occurs when consumers hesitate when faced with one type of product from various brands placed in one display case, even though this product grouping aims to make it easier for buyers to make decisions, shorten time, and make transactions directly. But these doubts can be put to good use to grab the user's attention and lead to impulsive decisions.

This is following data on service users, who are dominated by women, and as many as 67.3% often make impulse purchases based on emotional decisions. The visual hierarchical structure provided by Shopee is following women's behavioral patterns and habits in shopping. As mentioned in the previous discussion, it has been around for a long time, even before the existence of e-commerce. Women like to shop around, see lots of choices, and tend to compare various products before finally deciding. The similarity or suitability of the user's psychological characteristics is what drives users to impulsive purchases based on emotional decisions.

Figure 8 Compare Interface in Remaining Limit and Total Credit Used Source: Nada, 2024.

This comparison shows that both services emphasize the user's remaining credit limit on the Paylater section's main page, while other sections within the section display the total monthly expenses. This phenomenon also occurs in the e-wallet section, where both services fail to display the total monthly expenses in the transaction history list. This can be identified as a service effort to influence user psychology. Displaying the users' remaining limit tends to calm them down during transactions. Instead of being aware of the small amount he's spent on it, he knows the remaining limit. So indirectly, this also encourages users to continue making transactions. Moreover, with the various discounts offered.

Adapting to user interests and preferences in identity fit can increase users' abilities to interact with services. The comparison of the special Paylater promo section for the two services demonstrates this. Tokopedia focuses more on promotions for electronic products; it even places electronic brands in the priority section of the page. Meanwhile, Shopee highlights discounts on skincare and fashion products on this page. This enhances the persuasive appearance of Paylater services on Shopee, making them more relatable to the majority of female participants. The service aligns its display with the item categories that users typically favor and utilize. Therefore, attracting user attention during transactions is made easier. This condition is in accordance with the distribution of existing data, which places Shopee Paylater as the most widely used service, with the categories of goods most purchased with Paylater, including the skincare and fashion categories. Of course, the user's familiarity and connection to the main platform, which has existed for years, also plays a significant role.

Stages of Behavioral Design in Paylater Service

In comparing and mapping user interaction patterns, it is necessary to understand the triggers for the behavior's formation from a behavioral design perspective. This study aims to analyze the factors that form user behavior patterns when interacting with each service, and to identify similarities and differences between each platform that significantly influence consumer behavior. Therefore, it is necessary to identify touchpoints in the transaction flow of Paylater services in emerging marketplaces in Indonesia. Identify more deeply designed elements as persuasive design tactics that can change user mindsets and decisions in transactions.

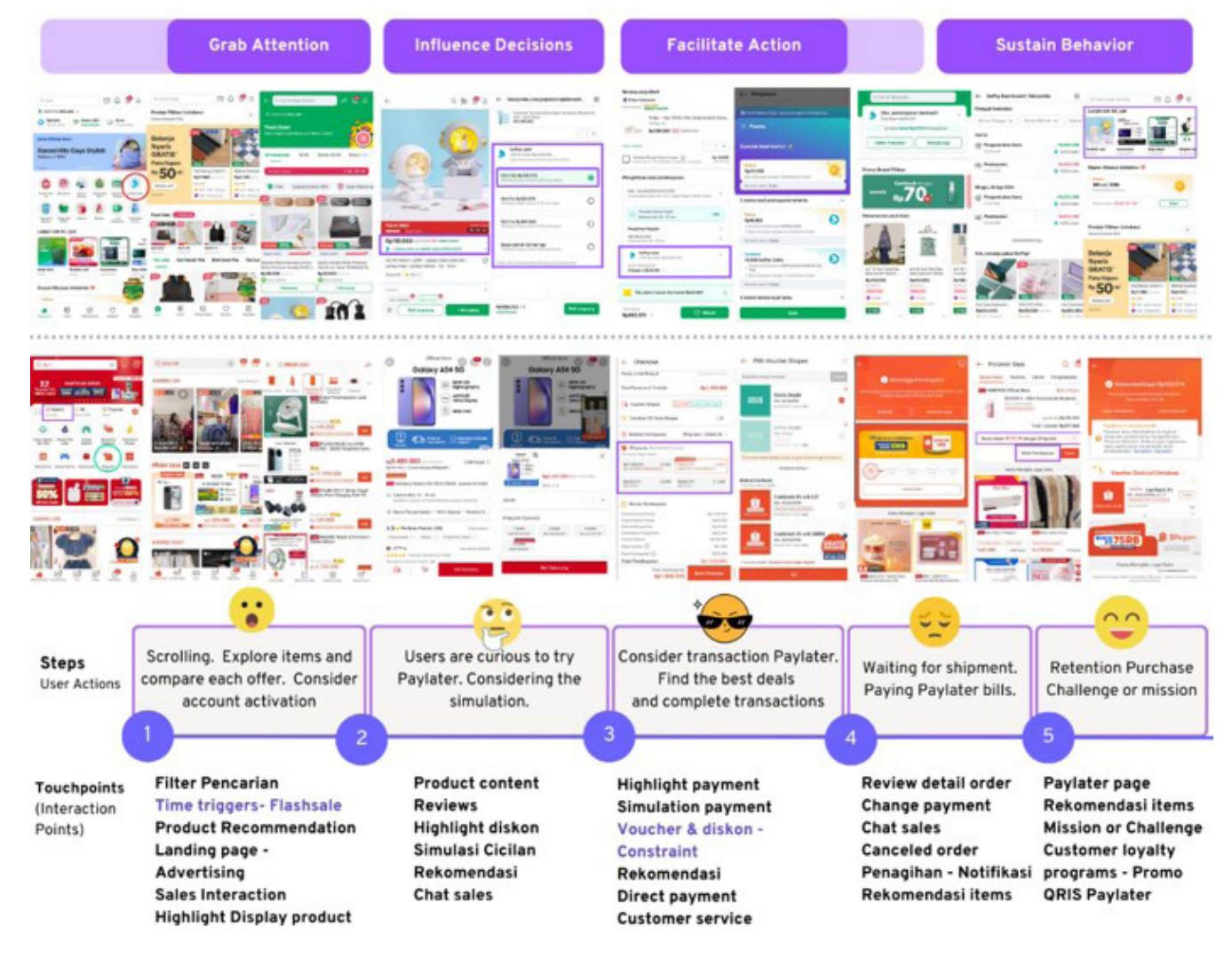

Figure 9 Overview Mapping Interaction Stages Source: Nada, 2024.

The user mapping illustrates that the Paylater service flow in the marketplace includes phases of behavior modification. According to Otani (2018), the four steps of behavior design are to grab attention, influence decisions, facilitate action, and sustain behavior.

Grab Attention

The design strategy aims to increase user awareness and foster user intention. At this stage, interactive services, a wide range of product choices, and the engaging product exploration process attract users, particularly women. Personalized content that caters to the user's interests and behavior towards the displayed item categories elicits emotional reactions such as surprise, curiosity, or urgency.

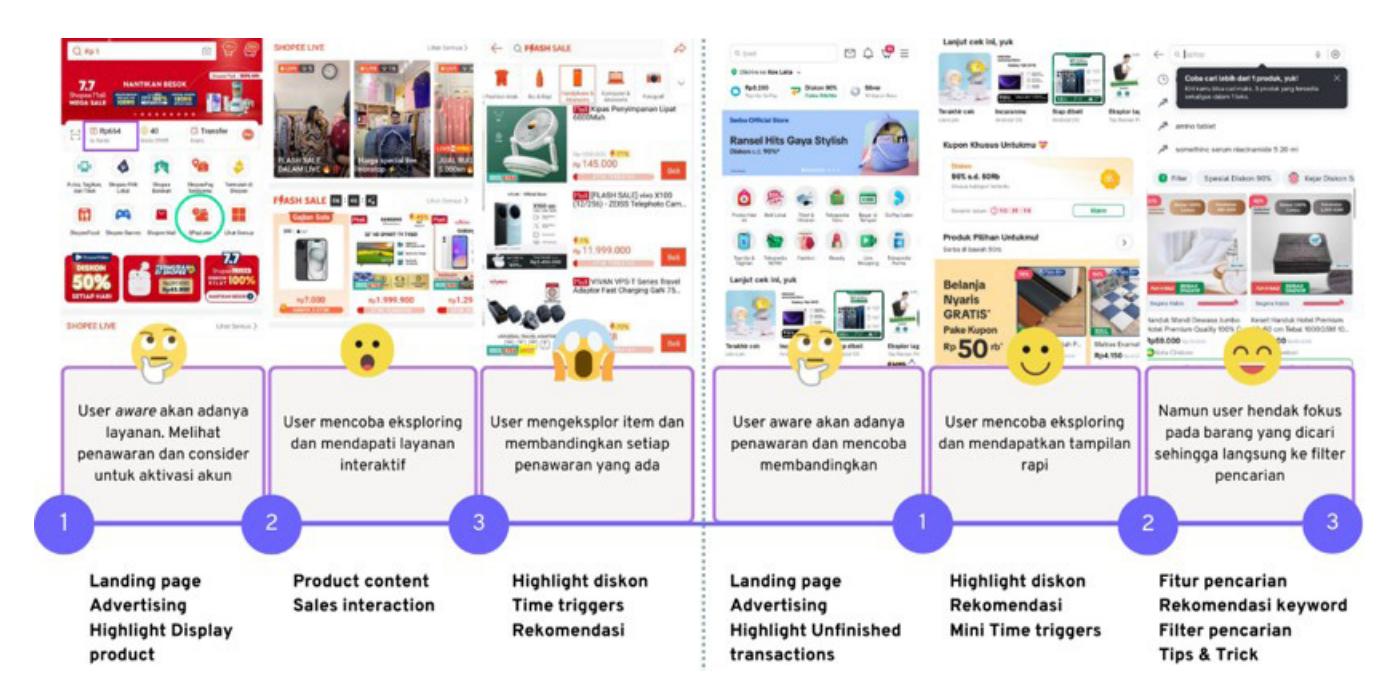

Figure 10 Comparative Touchpoint Interactions at Exploring Platforms Source: Nada, 2024.

The persuasive elements in the transaction flow significantly influence user decisions. The data from the interaction flow of the two platforms revealed different interaction patterns for each service. Differences in flow strategies and service priorities have a significant influence on their contribution to changing consumer behavior. Shopee typically utilizes interactive features like ShopeeLive, Flashsale, and ShopeeVideo to grab users' attention at the beginning of the page, followed by product recommendations. Meanwhile, Tokopedia has adopted a different strategy, adopting a minimalist aesthetic and prioritizing recommendations for products that are currently on sale over flash sales.

The visual hierarchy of service interaction priorities revealed that the frequency of flash sales on Shopee significantly influences users, leading them to explore or scroll items until they encounter Paylater triggers. The existence of time triggers such as flash sales can encourage users to tend to impulsive buying. On Tokopedia, users often use search to explore goods because they find it more convenient, and it aligns with their focus on specific items.

In this context, we can discern marketplace strategies that aim to heighten user awareness throughout the exploration phase. Psychological cues, such as the buyer's paradox in decision-making, habits, and identity fit, serve as triggers in the display and flow of service interactions, encouraging users to leverage their abilities and engage with the service for longer.

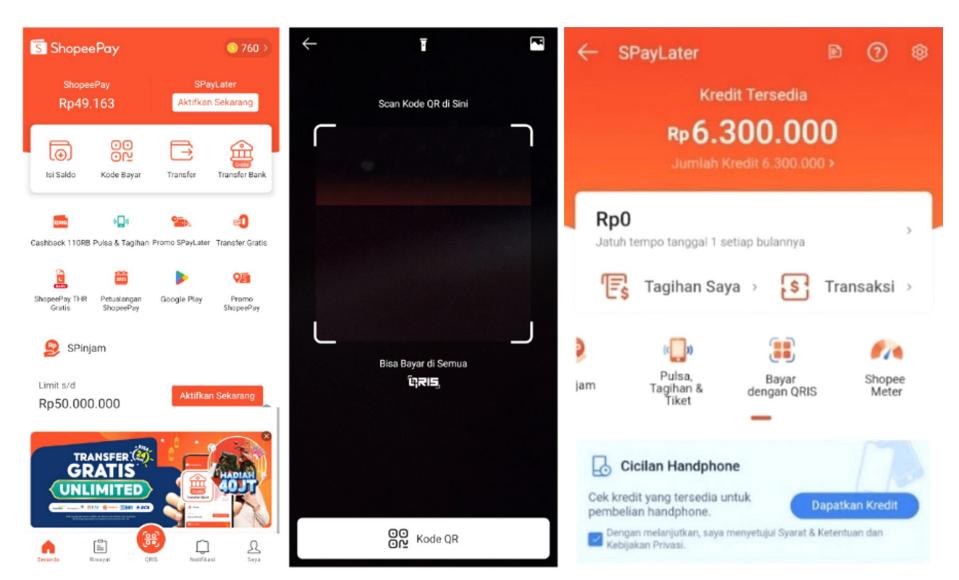

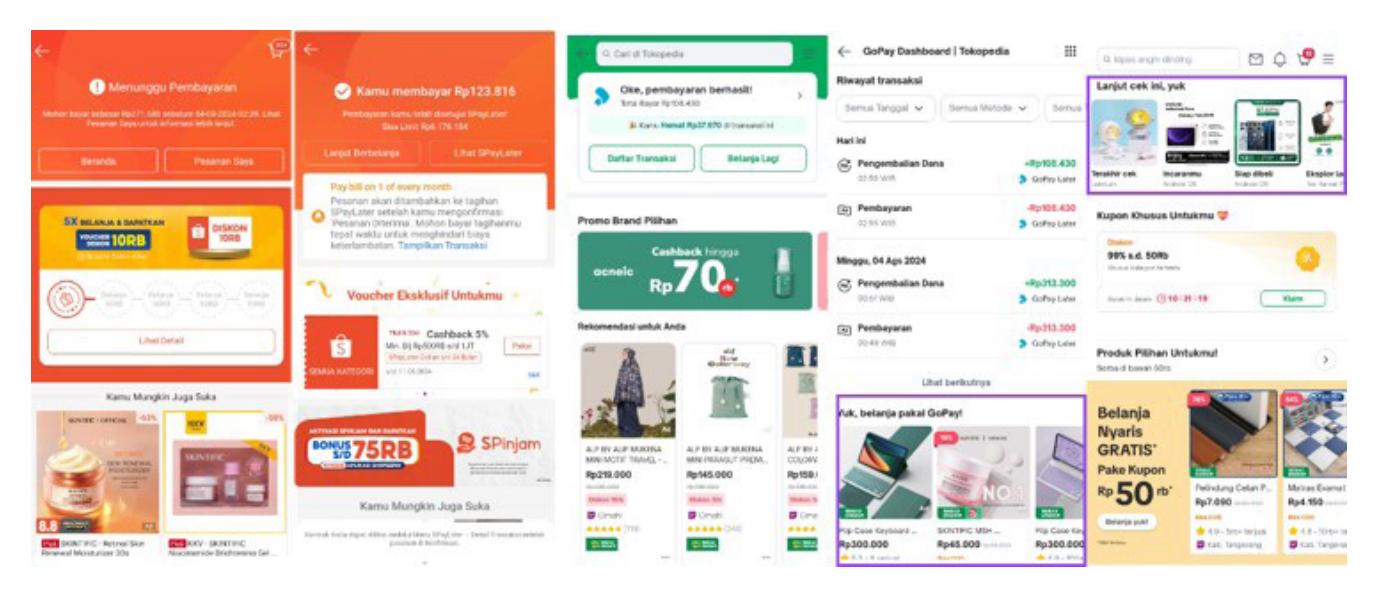

Influence Decisions

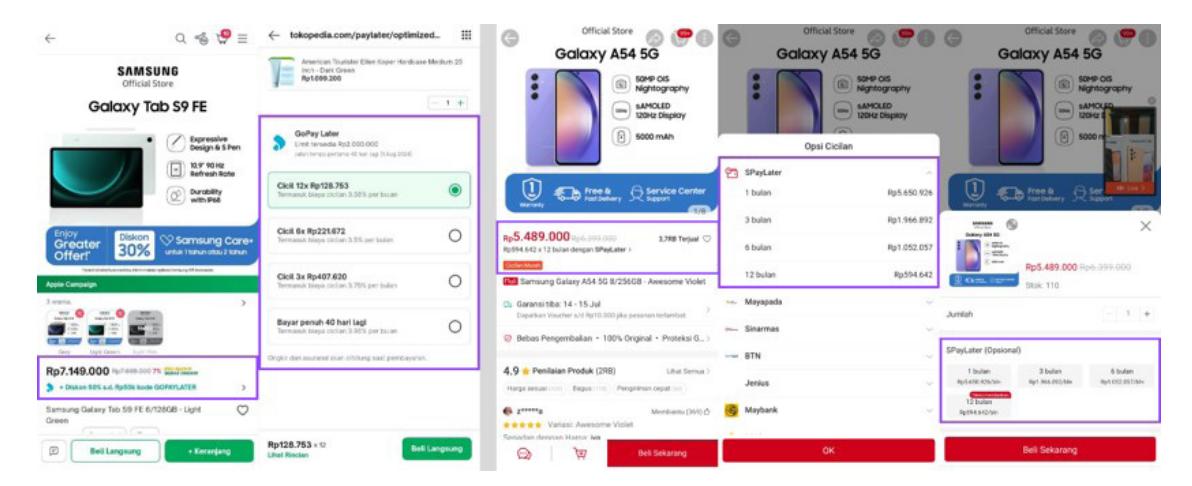

Once user awareness creates an intention, recommendations highlight the benefits of a specific action at this stage. The tunneling principle guides users through recommendations supported by affordances. Both services promote Paylater options, using cashback promotions to influence decisions. These services guide users to make plans that align with their financial capabilities by simulating experiences and providing tailored payment options, thereby simplifying and improving the suitability of the decisionmaking process.

Figure 11 User Interface at Detail Product and Simulation Credits

There are differences in the interaction flow in the installment simulation section. Tokopedia creates the installment simulation section separately and prompts users to act immediately on the recommended choices. The system will immediately direct the user to the checkout section. In the Shopee section, the simulation of an installment takes the form of a pop-up window that only displays installment details and doesn't allow for any other actions. Therefore, the user must close the pop-up again and proceed with the checkout process, just like they would with a regular purchase. However, the Paylater installment option is permissible because it includes the product type in the checkout basket. This indicates Shopee's efforts to attract and influence more users toward the installment option. Shopee's default user interaction familiarizes users more with the checkout process than the installment simulation, which they often overlook. However, when it comes to the steps and actions involved, Tokopedia excels in this particular area.

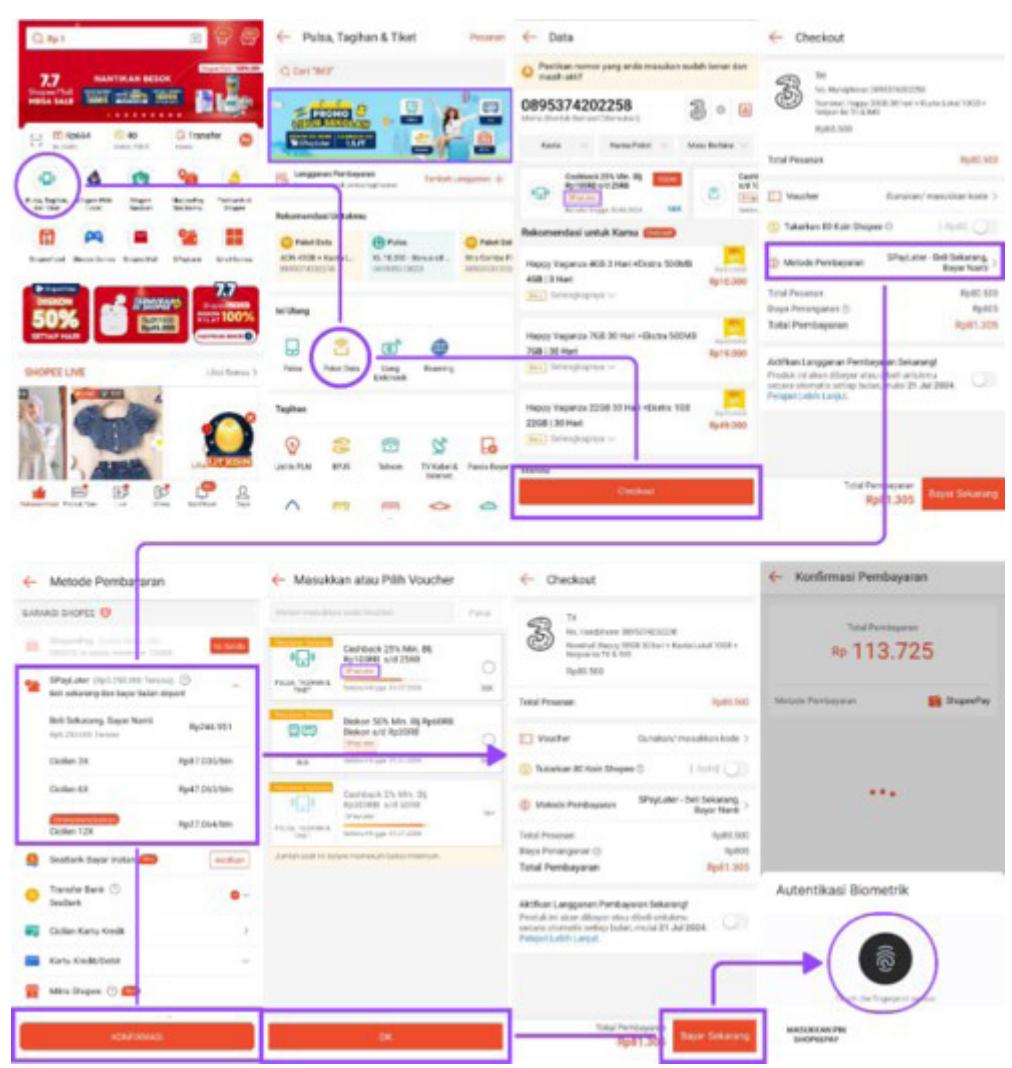

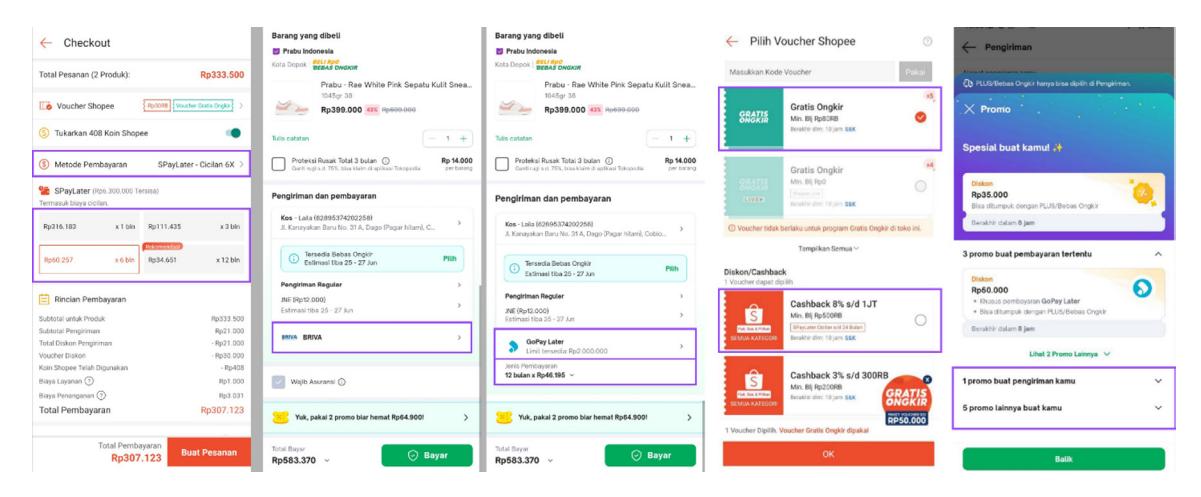

Facilitate Action

The facilitator action process, as previously noted, divides user interaction into several stages. Beginning with the transaction on the checkout page, users can access the payment confirmation, the package delivery process, and the invoice credits until they successfully complete the credit payment. From there, users encounter numerous impressive touchpoints, such as limitations on voucher or discount choices, a review of order details, the ability to modify payments, chat sales, canceled orders, reminder notifications, item recommendations, and more. Each of these elements serves to facilitate and simplify user behavior during transactions, thereby increasing user motivation.

Figure 12 User Interface Check-Out Page Source: Nada, 2024.

At this stage, the design ensures that users take the action goals. For instance, the design offers a credit simulation that features a marked discount. With the available options, users can tailor their loan requirements based on their individual conditions and abilities. The mapping reveals that Shopee's stepby-step process is more effective than Tokopedia. The user can choose the installment period during the checkout stage, alter the payment method, or cancel the order.

Figure 13 Payment Confirmation and Order Adjustment Source: Nada, 2024.

Following checkout, the design should verify the user's action using biometric authentication or pin payment and enable customization to alter the payment method or cancel the order. This is particularly important because, according to the collected data, 32% of participants selected the incorrect payment method. Some of them don't realize it until the transaction is successful. With the existing capabilities, users who often lack decision-making skills could adapt their needs when using the service.

Then it is related to interaction touchpoints where user expectations do not meet the services provided. One of these touchpoints occurs after the user has successfully checked out. Users expect that the service will display detailed costs related to the bill immediately after the transaction process is successful. However, the display occurs only after the user receives the item.

Many touchpoints from previous interactions did not meet user expectations at this stage. Both services, particularly the checkout stage, demonstrate success. The lack of initial display of the total costs was one of the most common complaints from participants. Users expect that the service will display detailed costs related to the bill immediately after the transaction process is successful. However, the display occurs only after the user receives the item. The second issue pertains to bills that persist even after canceling the order. The issue pertains to service policy, yet there are deficiencies in user education, accessibility, and information clarity.

This shift in behavior not only involves action, but also involves a sustained process of building long-term relationships through personalized and sustainable interactions, which are facilitated by signals and facilitator triggers such as challenges, rewards, or investments. Along with this connectivity, the process of forming habits becomes easier and influences user behavior more effectively.

Sustaining Behavior

Service efforts revealed various strategies for sustaining behavior, building relationships with users, and motivating them to keep returning to transactions. Shopee prefers to place touchpoints after transactions or bill payments with influence on Paylater challenges or missions to increase limits or get benefits such as coins. On the other hand, Tokopedia primarily utilizes user history for service exploration, highlighting incomplete transactions on both the main page and the e-wallet section.

Figure 14 Comparison Persuasive to Retention Behavior Source: Nada, 2024.

The similarity between the two services lies in their attempts to persuade users to return to transactions by presenting relevant product recommendations for each user who completes a Paylater or regular transaction. Occasionally, this can lead users to reconsider their decision and shift their order to a different shop due to a more appealing price comparison.

Both services also place a special Paylater promo section in the menu on the main page. Even though the promo is currently running, its effectiveness is diminished as users rarely interact with this section. Users explore more product showcases in search, flash sales, or focus directly on the checkout stage to compare prices. From there, we can identify a more effective strategy to sustain users' behavior, which involves highlighting the installment method on product item cards. It will be more effective if placed in the flash sale section, according to data on the effectiveness of triggers for users. So, users can more easily compare items and stores without having to look at the product details one by one.

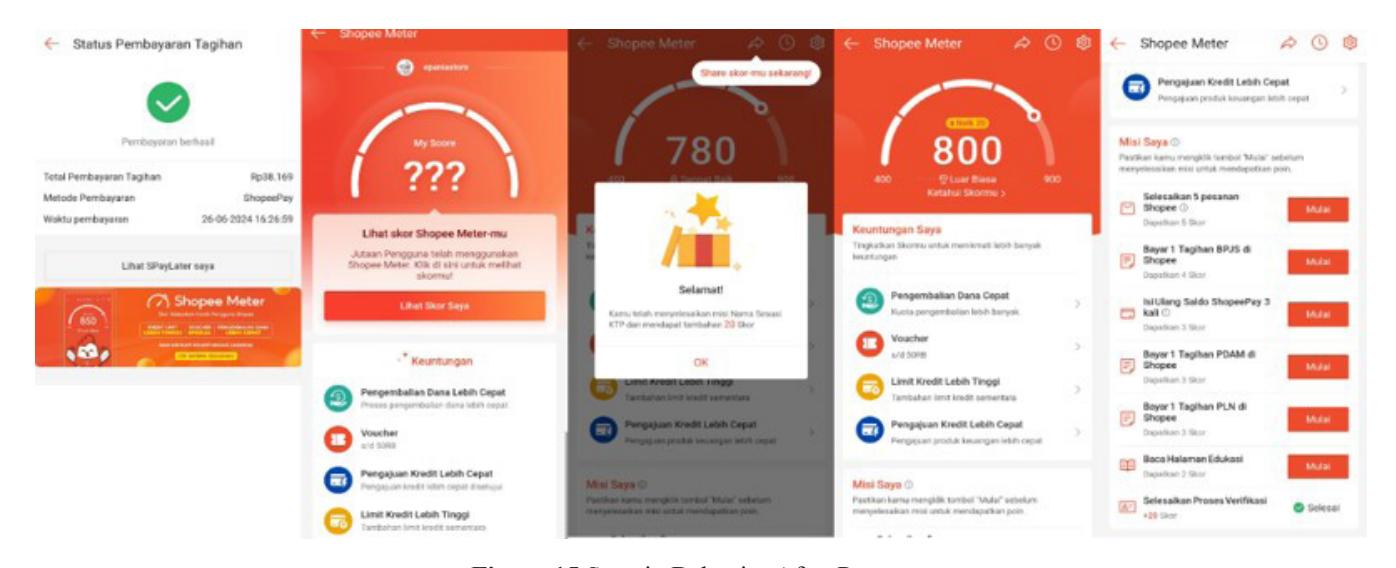

Figure 15 Sustain Behavior After Payment Source: Nada, 2024.

After paying the bill, Shopee tries to insert rewards and investment triggers. Shopee directs users to the Shopee meter section. Users must complete several challenges in order to access the offered benefits. Meanwhile, in the dedicated Paylater section, a separate challenge or mission center encourages users to complete orders using the Paylater method. The goal of this Shopee Paylater mission is to acquire coins. Of course, this challenge will influence user actions and motivation to carry out transactions. The more users experience these interactions, the more effective they are in forming user habits.

Studies reveal that the features of pleasure involved—games, coins, and challenges on Shopee are also quite influential in building user engagement with the service. Users often update their profiles and levels to unlock larger limits than before. It is known to be effective in influencing the frequency of use of Paylater on Shopee, which reaches 2-3 times a month. Meanwhile, on Tokopedia and Gojek, users tend to use it at certain moments or discounts.

The persuasive technology concepts applied to the appearance of each service can be different from each other. This results in distinct interaction patterns, tailored to the user's internal circumstances. The affordances and constraints of each service significantly influence the way users interact with it. Therefore, we can determine the optimal design strategy for navigating Paylater services integrated with e-commerce platforms at different stages of change.

Mapping Transition User Behavior Patterns in Digital Transactions

The service's efforts to influence users have changed many user decisions. Each designed flow has been identified as providing a trigger and directing users to transactions with Paylater and slowly causing a shift in user behavior in interacting with the service. The following is a mapping of various situations of shifting user behavior patterns that are currently emerging with the existence of Paylater services on various platforms.

Transition User Habits in Using Credit Payment

Habit is known to be one of the elements that drive a user's ability to achieve an action. If you look at the background of user habits, there are interesting conditions related to them. Before the Paylater service existed, 84.6% of users did not have the habit of borrowing. Prior to the existence of this service, customers had never previously used credit to purchase products from shops or supermarkets. This suggests that this service has the potential to alter users' purchasing habits for essential items.

The process of changing a user's behavior when using Paylater for transactions begins with their interactions with products; 94.3% of respondents have a habit of scrolling through e-commerce goods. 49% of them start their item search with no specific goal in mind. Just want to look at things. From that point on, users encounter numerous influencing factors associated with Paylater discounts, which subsequently guide them towards their final decisions. This aligns with the psychological tendency of users to seek the best deal when making transactions, thereby expanding their options and creating a persuasive flow of services. Users are curious to try the discounts offered with small transaction amounts; then this habit becomes capital as an ability to reach various types of transactions, thus encouraging impulsive buying and the use of Paylater in purchases. By implementing strategies that adapt the interaction flow to the psychological characteristics and behavioral patterns of users during transactions, we can simplify the service process of directing users.

Dependence on Digital Transactions and Paylater

In addition to the phenomenon of impulsive buying behavior, previous research has identified cases of online shopping addiction as a depressive disease, primarily due to consumption from traffic traps in e-commerce (Chengyu et al., 2024). Dependency indicators, according to Kotler & Armstrong (2016), consist of usage, feelings, usefulness, ease of access, and anxiety. Further examination reveals the following diagram, which describes the changing aspects of user behavior.

Since the pandemic, e-commerce has become increasingly popular. Based on a survey conducted, more than 50% of users feel dependent on online shopping on e-commerce platforms. This suggests that even in the absence of distance restrictions, this dependency persists. Changes experienced by users

include shopping online more often than in person, sometimes impulsive buying or shopping without careful planning, and carrying out transactions almost every day on e-commerce platforms; some of them are at the stage of feeling that they cannot meet their needs without e-commerce.

User anxiety can arise at certain moments, such as flash sale events. Large price discounts with specified time limits encourage users to be more competitive in transactions. Some users even resort to using bots to obtain items they don't actually need.

62.6% of respondents reported using ShopeePay more frequently than their primary e-commerce service or e-commerce itself. This suggests that users now consider e-wallets a daily necessity and prefer them over online purchases made through the e-commerce platform itself. Sometimes, due to certain considerations, users choose to shop at malls or supermarkets instead of e-commerce, but they still use e-wallets or QRIS for their transactions.

In this situation, there is a tendency for user dependency on e-money to be greater than e-commerce. Data related to user dependence on digital transactions, reaching 74.3% of all respondents, reinforces this. However, the impact of another 22.9% was minimal. This stands in stark contrast to the reliance on e-commerce, which only accounted for 50% of all respondents, as previously discussed.

58.97% of participants in an open survey on the X media platform felt that using cashless money increased their consumption. Users only become aware of the expenditure when they check their balance, as they don't physically feel it. Furthermore, the transaction process is simplified by simply scanning the QR code on QRIS, eliminating the need to physically visit an ATM, even if you don't have a wallet with you. Meanwhile, 41% of respondents still perceive cash as a more convenient method of payment. Because of the environmental conditions, more people accept cash payments, making cashless transactions considered more economical.

According to the latest data, it is known that e-wallets have become the most popular payment method in the last year, reaching 84.3%. Meanwhile, the use of Paylater has increased by one level compared to the previous year, but it still lags behind transactions via Alfamart or Indomaret, at 45.9% compared to the previous 27%. Thus, the use of Paylater has increased quite rapidly and has now exceeded the use of credit and debit cards and even payments through the nearest minimarket. This indicates a shift from physical to digital payments, especially in lending methods.

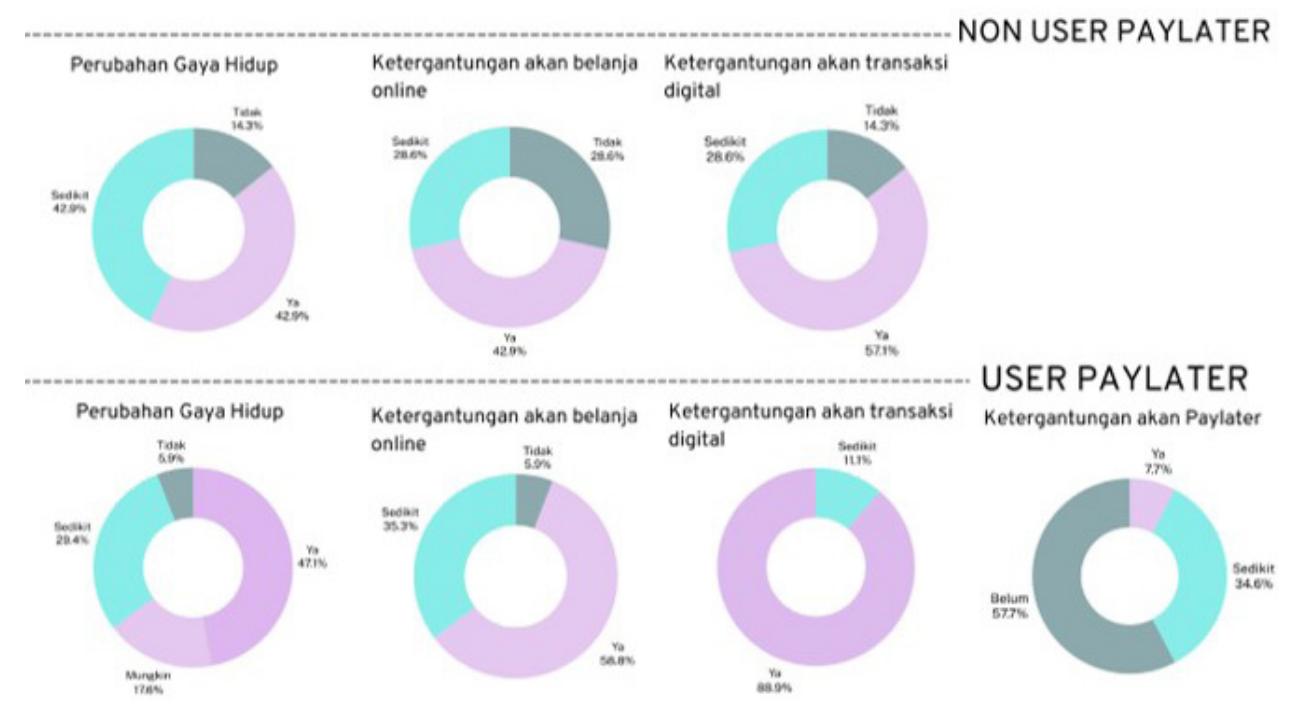

Figure 16 Data User Behavior Changes Source: Nada, 2024.

Paylater users exhibit significant behavioral changes compared to non-users, with Paylater users being more dependent on e-commerce, digital e-wallet transactions, and lifestyle changes. 67.3% of Paylater users make emotional decisions and change their minds after seeing offers to use the service, suggesting it can alter purchasing habits and help users acquire items they need. The marketing strategy incorporates persuasive elements to guide users towards these options.

11.8% of Paylater users experience dependency, with 35.5% currently experiencing slight effects. Users use the online loan service monthly and make transactions more frequently than regular payments. Some feel they cannot fulfill their needs without Paylater, validating the current state of user consumption patterns. The possibility of using Paylater is increasing and has the potential to completely replace credit cards.

The current state is influenced by a cashless society, shifts in credit service users, changes in credit habits, and online loans for consumptive behavior and impulsive buying. There is an increasing reliance on e-commerce, e-wallets, and Paylater services for digital transactions. These implications and behaviors occur without intervention from a service that alters the structure and social hierarchy of the interaction process.

Design Relations in Influencing User Behavior on Paylater Services

This research explores how user internal conditions, such as familiarity, task knowledge, daily use frequency, habits, and beliefs, shape their interactions with services like Paylater. User activities like scrolling, promo hunting, daily QRIS transactions, and check-in routines increase exposure to persuasive elements. Financial constraints and social environments that favor Paylater further condition users to view it as a viable solution, driving their engagement with the service.

From the service perspective, product attributes, including appearance and interaction design, play a crucial role in shaping user behavior. Psychological cues align with users' characteristics, making the persuasive process more effective. Interaction flows incorporate stimulation, evocation, and manipulation techniques to prompt user actions, using the triad functionality principle to understand how technology influences behavior.

The analysis identifies several critical user needs and challenges, such as careful placement, sizing, and contrast of elements, facilitating user navigation, and clearly communicating changes in service provisions and policies. To address impulse buying behavior and prevent transfer errors, daily or monthly transaction limits are required for e-wallet and Paylater services. Additionally, providing an option to temporarily deactivate unused accounts enhances security and informs a more effective design strategy for e-commerce platforms integrated with Paylater options.

In a cashless society, user behavior has shifted significantly, with many users becoming unaware of their spending habits. The Paylater system effectively attracts a younger demographic, including students without fixed incomes, fostering inclusivity and resulting in more frequent credit purchases. The service's efforts to influence users have changed many user decisions, leading to increased reliance on e-commerce and Paylater services in digital transactions.

Conclusion

The Fogg Behavior Model framework and functional triad model are used to analyze the effectiveness of persuasive technology in the development process. The research focuses on the stages of behavioral design in Paylater, including building user attention, influencing decisions, facilitating action, and sustaining behavior. The grab attention process often leads users to explore services, but touchpoint interaction on the checkout page, particularly discounts, is more effective. Time triggers or flash sales are more effective in influencing transaction intensity, especially for impulsive buyers. Discount constraints at the checkout page lead to more retention purchases and final decisions to use Paylater.

Persuasive design elements are related to psychological cues from user characteristics, which influence buying decisions. This research identifies a gap in the best design strategy for navigating Paylater services at Marketplace. Future research should implement structured experimental user testing to measure behavioral changes during service interaction and analyze various scenarios. Future research could integrate behavioral design to empower communities, establish new patterns, and enhance user interactions across service categories, such as public health, government services, and children's space or education, to develop a better impact.